Student accommodation trends: your questions answered

Image courtesy of Adobe

StuRents’ Annual Webinar: Q&A Highlights, Attendee Poll and Top Student Rental Sector Trends

The student rental sector is undergoing significant change, driven by shifting demographics, economic pressures, and new regulations. Our StuRents Annual Student Accommodation Report 2024 and annual webinar, StuRents Insights: A Year in Review, explored these trends at both national and city levels.

While national PBSA rent growth is strong, city-level variations and rising Build-to-Rent (BTR) competition, alongside the Renters’ Rights Bill, are reshaping the market. Students face increasing financial pressure as rent growth outpaces loans. Higher-tariff universities continue to attract international students, but factors like exchange rates and inflation in key markets are slowing growth.

Explore our Q&A and poll analysis below for a closer look at the forces shaping the student rental sector’s future.

Annual Webinar Questions and Answers

Q: There have been reports that entry requirements for Chinese students were raised last year and subsequently fewer Chinese students are coming to study in the UK. Is there any basis to the claim, and if so, should we expect this trend to reverse in the upcoming academic year?

Entry grade requirements will vary per institution, but anecdotal evidence suggests changes to these have fluctuated both up and down depending on the university. As we saw during COVID, prestigious universities are arguably more insulated from reductions in overall demand due to their ability to change these requirements and take market share, given the flight to quality trend.

Q: Which cities are currently struggling, particularly with voids and oversupply?

Recruitment volatility has been a theme over the last few years. Those universities which were overexposed to countries where demand has faltered, such as Nigeria, will have been negatively affected. Additionally, it’s rare that supply and demand growth in any given year is aligned. As we have seen in cities such as Nottingham, PBSA growth was significant in 2024, leading to a deterioration in fundamentals.

Q: For Chinese students, has there been any price point change from 22/23 to 23/24?

Whilst there will be additional contributing factors such as the performance of individual operators and locations if considering listing views (properties being clicked and viewed on StuRents.com by Chinese students) the average price viewed outside of London increased by just 3.0% year-on-year. This was down from double-digit growth reported in the previous year.

Q: What is the view on the number of international students for the September 2024 cycle vs last year?

There remains a lack of live demand data covering the whole of the international student market. Year-on-year changes will very much depend on the demographic, for example, currency fluctuations have led to a significant fall in demand from Nigerian students. While the latest UCAS data shows an overall drop of applications and acceptances for international students, there was a small 0.7% increase in applications this year for Chinese students.

Q: How is demand varying between Russell Group cities and non-Russell Group cities?

Considering only cities in England containing a Russell Group institution, and excluding London, according to the latest data from the Office for Students these Russell Group cities reported year-on-year growth in both postgraduates and undergraduates. In comparison, non-Russell Group locations reported noticeable declines in postgraduates.

Q: With upcoming legislative changes such as the Renters’ Rights Bill, are PBSA operators concerned about a potential migration from their schemes to BTR schemes?

The market is certainly starting to pay attention to BTR, driven primarily by the developments in Leeds this year. The exact impact is hard to quantify and will depend on the specific asset in question, with price, location, unit size, and amenities all contributing to whether a student will ultimately decide to live in PBSA or BTR.

Q: Operators and investors are wishing to see year-on-year revenue growth despite lower than expected occupancy in the 24/25 academic year, with indication that rooms were too expensive. How can revenue growth be sustained in the 25/26 academic year?

Knowledge is key. Investors need to be realistic about their expectations. For example, 2-3% growth was the norm pre-Covid. Recent rental growth would have taken 5+ years under ‘normal’ circumstances but this growth was compressed into a couple of cycles. Revenue increases can only be sustained where demand is high and supply constrained. As we have seen in locations where alternatives such as BTR are available and rents are competitive, this will pose a challenge to PBSA schemes.

Q: Which locations are you seeing an undersupply in student accommodation relative to the demand, taking into consideration the pipeline in planning?

Shortages in Glasgow have been well reported over the last 12 months. However, the market has responded and a significant number of planning applications have been submitted in recent months. London remains challenged from a supply perspective, but high rents limit the addressable market for new builds.

Q: Are you seeing an increase in the number of studios in the pipeline across the UK (as % vs. clusters)? If so, is this being driven by demand, or by developers trying to stack an appraisal?

Certainly, a larger proportion of beds submitted over the last 1-2 years have consisted of studios compared to historical levels. Whilst there is a general need for more accommodation, developments and the units being proposed are not always matched to where the need is greatest. This is partly due to a lack of data when appraising locations but also the ability on paper to charge higher rents for studios, which makes the returns more favourable. Of course, this assumes these beds can be filled and there is a specific need for these types of units in the locations being proposed, which isn’t always the case.

Q: Some PBSA operators have been using dynamic pricing to encourage students to book early. However, closer to intake, available rooms are let at large discounts (compared to advertised early booking prices). Is this a common practice, and is it also a practice for HMO? What effect could we expect on booking seasonality?

This varies significantly per operator, with some taking a very active approach and others not. Not all property management software is set up to change rents in such a manner, as it can create a significant administrative burden. The 2024-25 cycle was certainly later than the previous year, resulting in some operators offering significant incentives or discounts. Unless demand picks up for 2025-26 there is a risk we could see the same again this year, with some savvy students possibly holding firm until such discounts become available.

Q: With little chance for PBSA to adjust rents downwards as students financially struggle more, we would therefore see more students having to look at HMO. What are your thoughts on the Renters’ Rights Bill legislation and its likely impact on reducing supply, potentially leading to more students attending their local university as they cannot afford to live away from home?

With domestic students equating to the largest proportion of demand, there is a need for additional, affordable accommodation, typically offered by HMOs. Whilst there is a lot to be commended in the Renters’ Rights Bill, there could be unintended consequences. Specifically, will landlords increase rents to offset the possibility of shorter tenancies? Equally, 2-bed properties, not specifically deemed to be HMOs, fall outside of the Ground 4a provision, meaning student landlords have no certainty of whether the property will be vacant in time for the new student cycle. These factors could lead to a reduction or consolidation of supply, however, supply-side pressures and rising rents are likely to lead to more students studying at their local university.

Q: The Renters’ Rights Bill will not allow advance payments, which is typical for international students. How would international students proceed in the absence of an in-country guarantor in this circumstance?

PBSA is expected to be exempt from these restrictions. However, Concurrent’s recent integration with Leap provides the option of waiving a guarantor in favour of a higher weekly rent, providing students with additional options.

Annual Webinar Attendee Poll

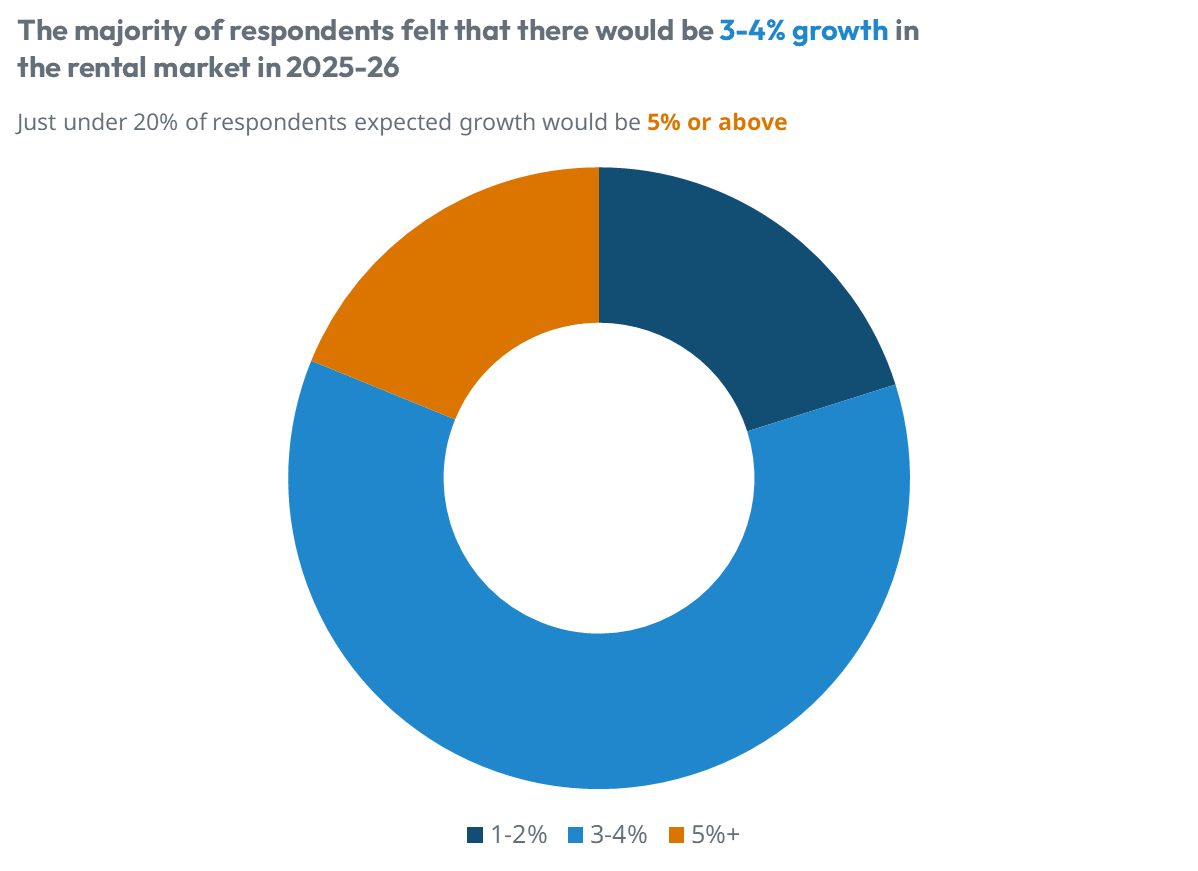

The first question posed to attendees was their expectation for rental growth in the 2025-26 period. Most respondents believed that there would be 3-4% growth, with 20% taking a more reserved view at 1-2%. Only 3% of attendees indicated an expectation of 7% or more.

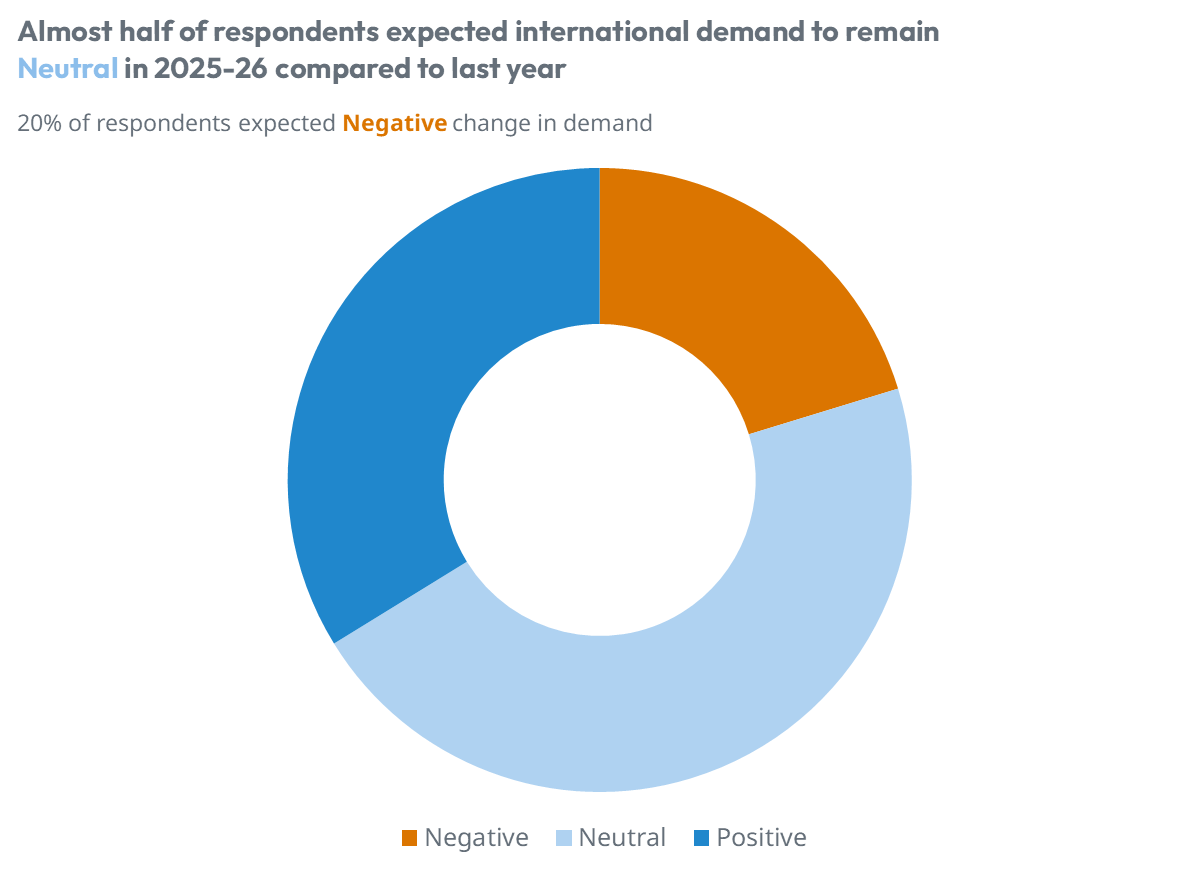

Looking at international demand, we then asked attendees about their expectations compared to last year. The majority expected demand to be neutral, with 34% believing there will be positive growth.

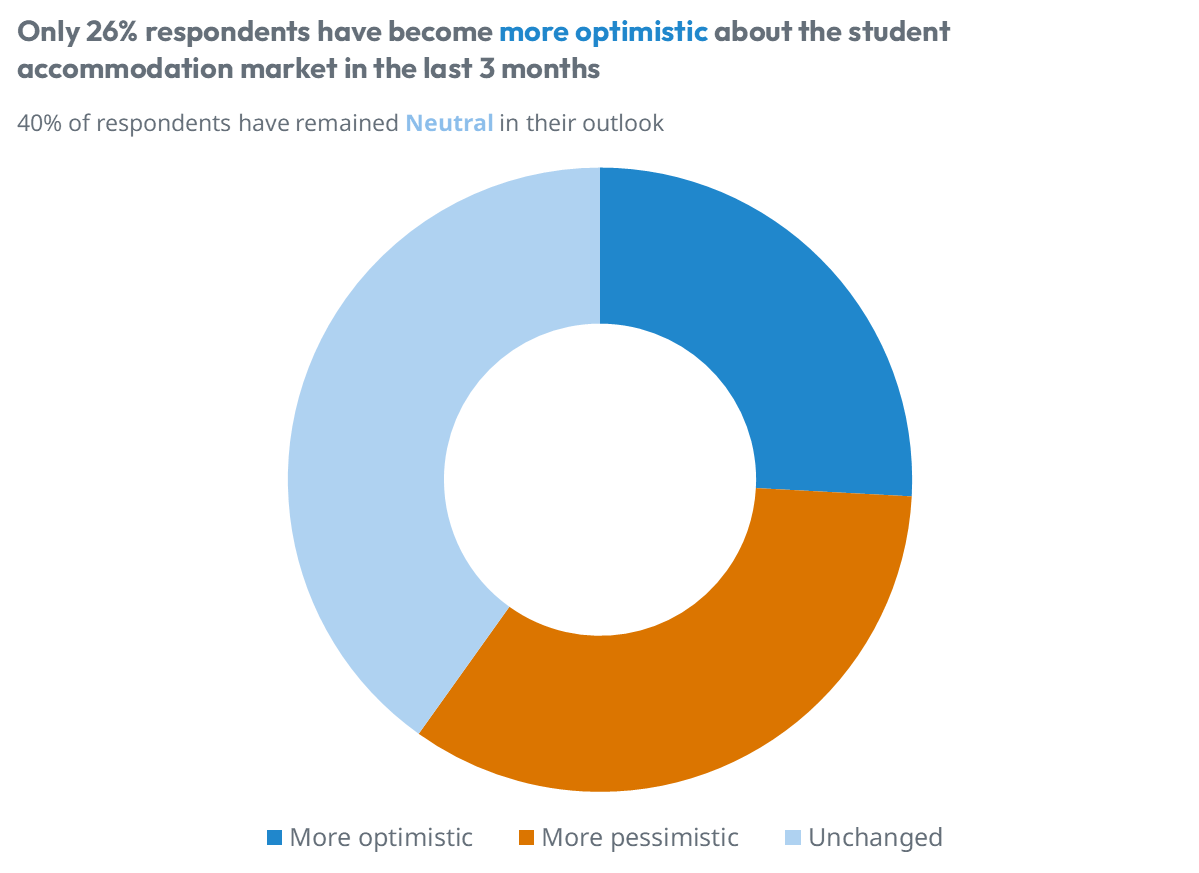

Finally, we asked attendees how their view towards the student accommodation market has shifted in the last 3 months. The majority indicated that it was unchanged, with 34% taking a more pessimistic view.

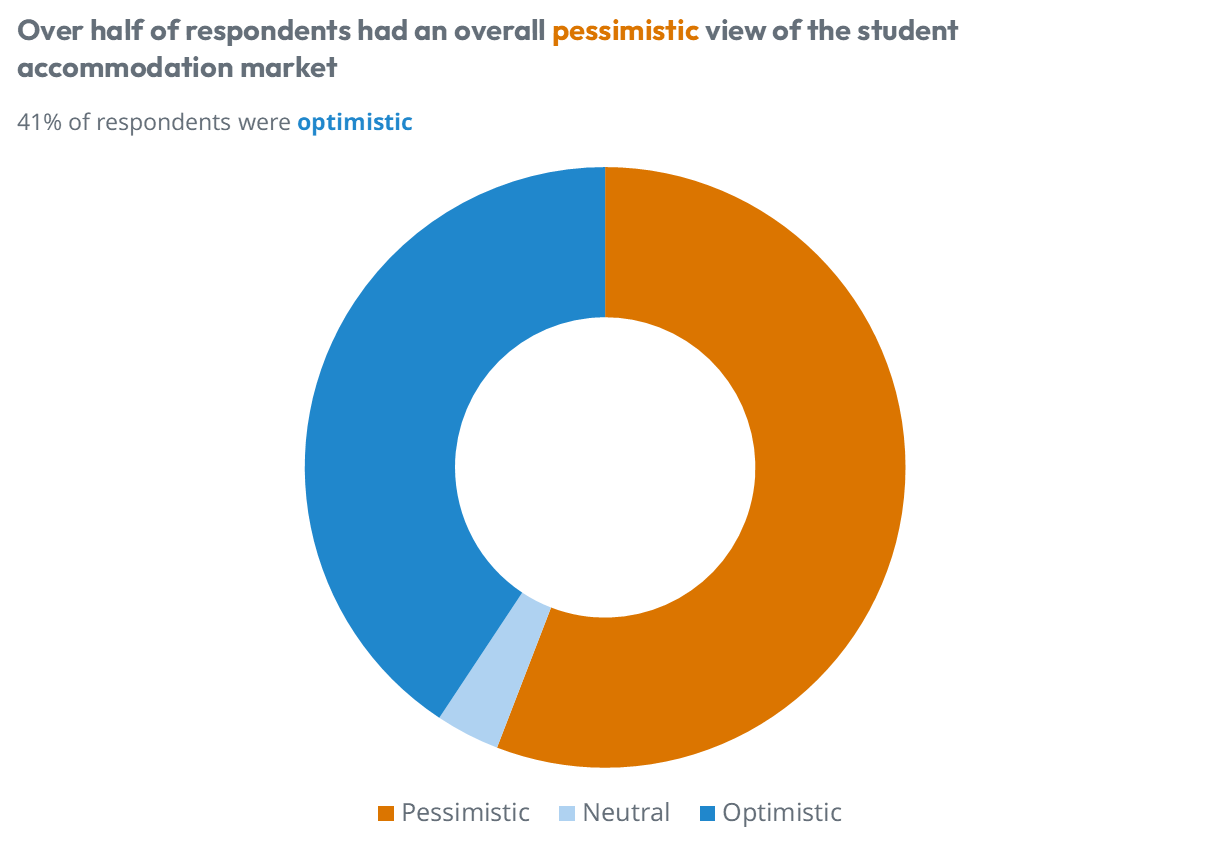

Taking an aggregated view of all answers provided (by assigning numerical values to optimistic, neutral and pessimistic responses), there was an overall pessimistic sentiment to the student accommodation market, with over 56% of attendees indicating negative or pessimistic sentiment across all three questions.

In conclusion, the student rental sector is navigating a period of significant change, driven by demographic, economic, political and regulatory factors. While uncertainties remain, the future of student housing holds opportunities for those who can adapt to these shifts, making it crucial to stay informed and responsive to emerging trends as we look toward 2025.

For more information about our proprietary, highly granular data covering UK student accommodation contact the StuRents Research team today. Or book a demo of our Data Portal to find out how you can have up-to-the-minute university housing insights at your fingertips.

Note: Webinar questions were edited for clarity.

Share

Article by

Research Analyst at StuRents

David Reader is a research analyst in StuRents’ research division, StuRents Intelligence.