2025 Forecasts for student accommodation

2025 Forecasts for Student Accommodation

With 2024 firmly in the rearview mirror, attention has shifted towards what to expect from the sector over the next 12 months.

We consider some of the headline trends worth watching this year.

Student demand

As we've discussed in previous sessions and covered in our 2024 Annual Webinar, last year was very much one of volatility, with slowing demand taking some by surprise given the bullish market trends post-COVID.

Whilst a lot of the rhetoric around international demand has been negative in recent months, it's worth putting this into perspective.

Leasing velocity for PBSA in 2024-25, whilst slower than the previous year, remained resilient at an aggregated level. StuRents Occupancy Survey reported PBSA schemes were 92.2% let in Nov for the 2024-25 cycle, down just 1.8 percentage points year-on-year. Of course, there will be huge city and scheme level variations but on the whole, PBSA continued to perform well.

Whilst occupational performance remained relatively strong, it was certainly harder to fill beds, with incentives and discounts much more widely used compared to recent years. For 2025-26, those students able to hold their nerve may decide to book later, in what could become a game of who blinks first. Early anecdotal evidence suggests there hasn't been a spike in demand, indicating it could be another slow year. This will likely lead to increased competition and a higher cost of acquisition. Of course, those operators participating in StuRents Occupancy Survey will be able to accurately assess how the market is performing, thus making more informed marketing decisions.

Build-to-rent (BTR) also raised its head in earnest last year and key markets such as Leeds and Manchester may come under increased scrutiny, as stakeholders try to establish the extent to which it is impacting PBSA. With limited BTR data available, we can expect demand for insights to increase.

For BTR operators with noticeable exposure to students, the question remains as to how it can wean itself off this demand pool, given the potential cliff edge of tenancies related to the student letting cycle. It will be worth keeping an eye on operators to see how they can manage this transition.

Development

The cost of development remains prohibitive, in part due to debt costs. Over the last month, these costs have risen again, with 5-year SONIA swaps rising to 3.923% at the time of writing, up from 3.604% a year ago. Higher borrowing costs are likely to negatively impact the number of projects being successfully funded, ensuring that the delivery of newbuilds will remain low in the medium term. Of course, in the longer run, any factors which could restrict the delivery of new stock will be positive for operational assets in the face of what could be a slower demand growth.

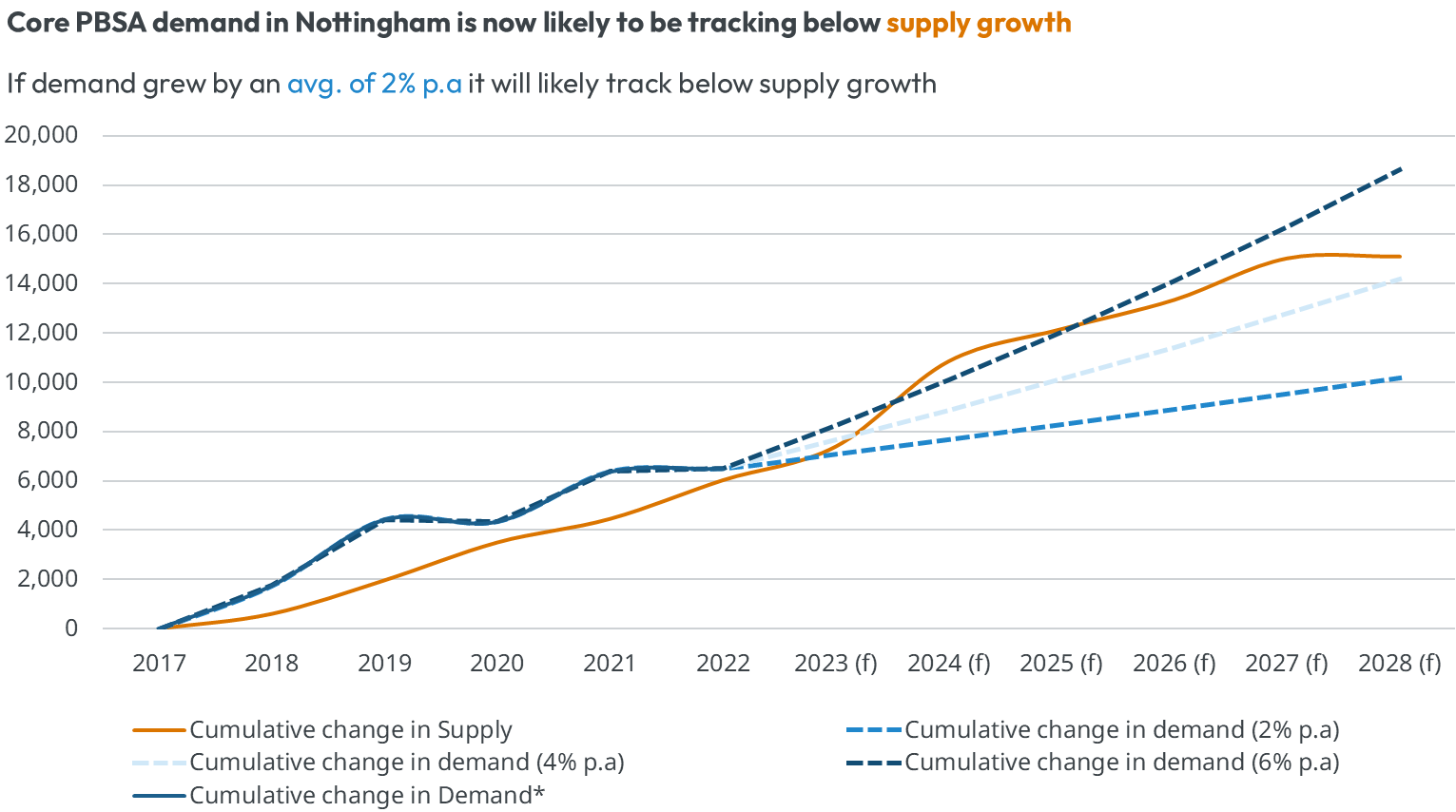

For 2025, those underwriting developments need to carefully consider future supply and demand and how this will impact the performance of an asset. For example, future assumptions around a city’s performance may not be realistic if only historical trends or blunt student-to-bed ratios are considered. As we have predicted through our supply vs demand analysis, markets such as Nottingham could face continued headwinds, which is in contrast to the fundamentals reported pre-2024, and which may have originally formed the basis of an investment case.

NB: Core PBSA demand excludes students living at home and returning domestic students as a significant proportion are likely to live in the HMO market. Between 2017-2023 demand was growing faster than supply, however, supply growth is now likely to be expanding faster than demand leading to increased competition between PBSA providers.

Planning including London

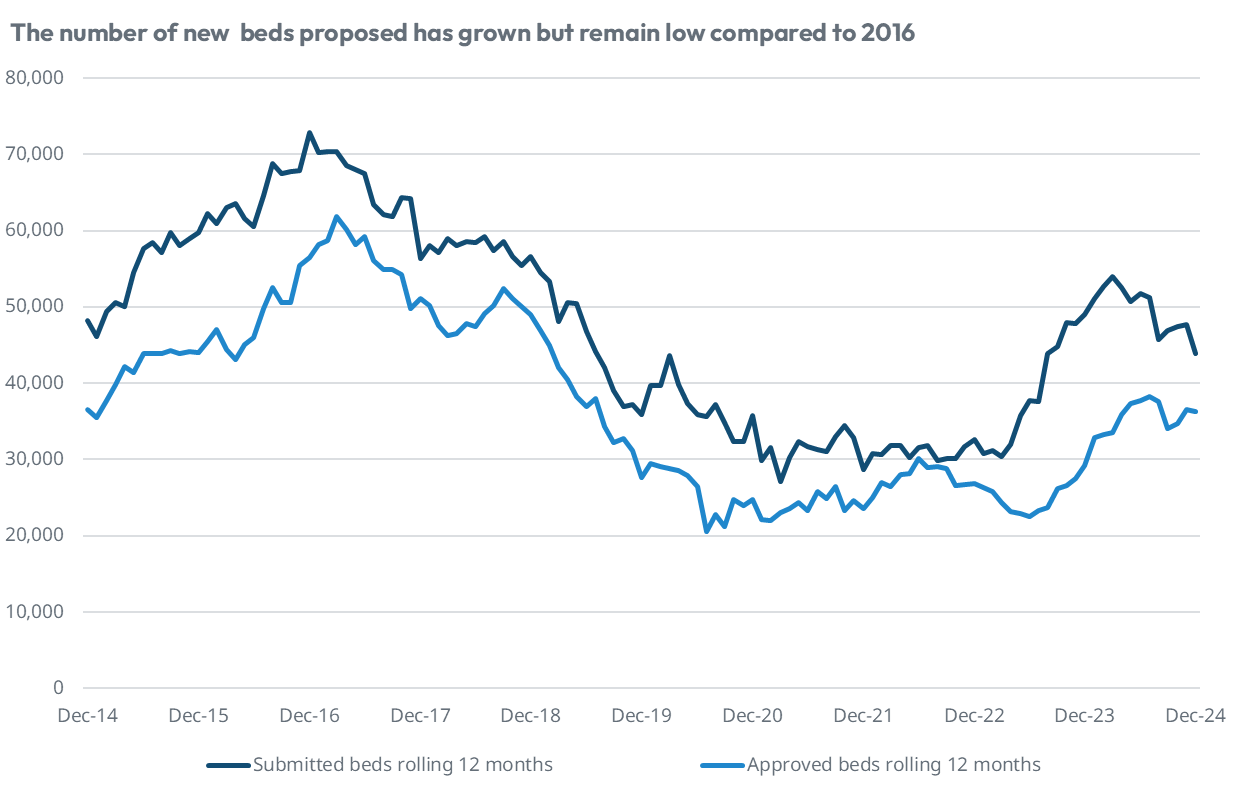

Planning activity is likely to remain up from the lows reported in previous years but will continue to be focused on the few viable locations where ‘achievable’ rents can support development. Meanwhile, the softening of the London plan at the end of last year could lead to an increase in projects proposed in London.

The number of schemes expected to be delivered in time for the new academic year will remain subdued. However, early data suggest the figure could surpass the volume delivered in 2024, although growth will vary significantly per location due to the uneven distribution of the pipeline. In Nottingham supply is likely to expand by more than 2k beds in 2025, following the ~2.5k added last year, representing substantial growth in just two years.

Rents

Pre-COVID, rental growth was traditionally ~2-3% and we are likely to see a reversal towards this trend this year, with of course winners and losers posting growth both above and below this headline figure depending on the specific location.

Whilst early house-hunting is dominated by domestic students, the average price being viewed by British students between Oct 24 and Dec 24 was up by 2.1% to £157.37pppw. This compares to year-on-year growth of 6.6% reported during the Oct 22-Dec 22 period.

Renters’ Rights Bill

The Bill continues to loom large over the sector. The most significant impact is likely to be felt in the HMO market, albeit there is still some uncertainty over how the legislation will affect PBSA.

Expect 2-bed properties to be impacted most significantly. Technically not HMOs, these properties are not covered by Grounds 4a of the Bill, which allows student landlords to regain possession of their properties to align with the academic year. These small houses can equate to a substantial proportion of supply but student landlords, as it currently stands, will have no certainty over the ability to regain possession of their property to ensure it can be re-let in time for the new cycle.

Whilst there are other important implications of the Bill, the ability to serve notice could lead to a sector which is typically dominated by 52-week contracts, seeing the average tenancy length contract. In response, some landlords are likely to increase rents to offset this risk, whilst consolidation or even contracting of supply could occur.

How long it will take for the full impact of the legislation to be felt is unclear, however, in a market with growing demand and a lack of affordable accommodation, there is an increasing risk that those from less affluent backgrounds will be priced out of higher education. This in itself could become a risk for the sector and has the potential to curtail expected demand growth.

For well-positioned assets in strong markets, operational performance is likely to remain positive in 2025, even if markets are later and in some cases down year-on-year. For others, in systemically oversupplied locations and weak demand growth prospects, the outlook is less rosy. As always, this highlights the importance of deep, unbiased, analysis of each location or asset. Strap yourselves in for what could be a topsy-turvy year.

For regular updates on the student accommodation market be sure to become an Insider by visiting StuRents.com/research

Share

Article by

Head of Research at StuRents

Richard leads the StuRents research team, providing proprietary, platform-driven insights to help stakeholders make better-informed decisions about the market.