PBSA Recent Growth & Potential Pipeline

Image courtesy of Unsplash

PBSA Recent Growth & Potential Pipeline

As we turn our attention to the upcoming academic cycle, it’s clear that interest in the UK student accommodation market isn’t showing any signs of slowing down. Despite the lingering uncertainty around international student numbers and the potential impact of the Renters’ Rights Bill, developers and investors remain optimistic about the demand for Purpose-Built Student Accommodation. This blog will explore what we might expect from 2025 through 2028, drawing on the latest planning application data and supply figures.

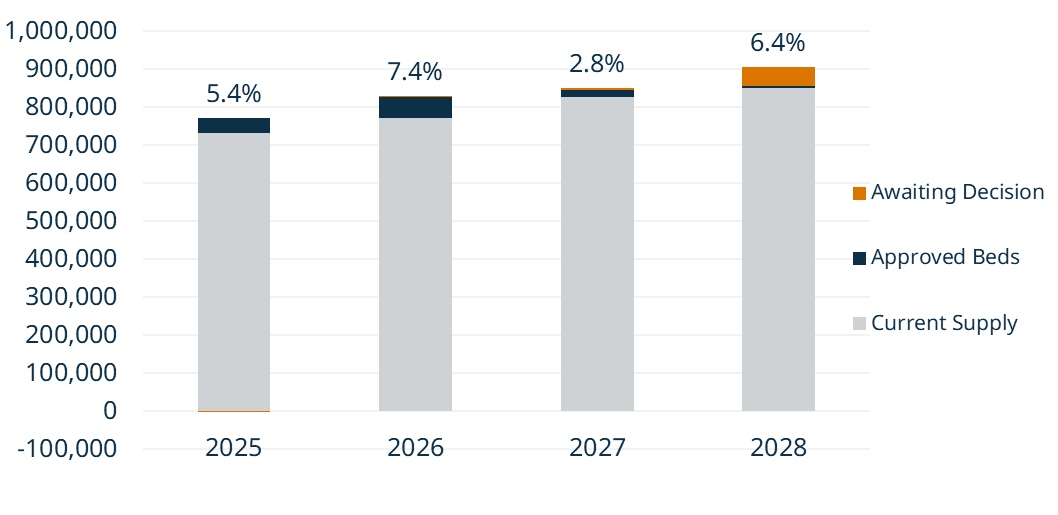

We begin with a high-level overview of the UK’s overall pipeline, offering a snapshot of the beds currently approved and those still awaiting decisions. Whilst it’s improbable the pipeline will be delivered in full, current data suggests that the sector could benefit from up to 120K beds over the next four years, with an additional 55K at various stages of the planning process. The chart below illustrates how these figures translate into projected year-on-year growth nationally.

Year-on-year growth could reach 5.4% in 2025, then accelerate to 7.4% in 2026 before dipping to 2.8% in 2027 and rebounding to 6.4% in 2028. It’s worth noting that not all projects in the pipeline will come to fruition. Factors such as the cost of debt and rising construction expenses can hinder development. However, the pipeline is also likely to expand as new applications emerge in the coming years.

Figure 1: National Supply Growth Potential 2025-28

Source: StuRents, all relevant local authorities

Growth Potential at a City Level

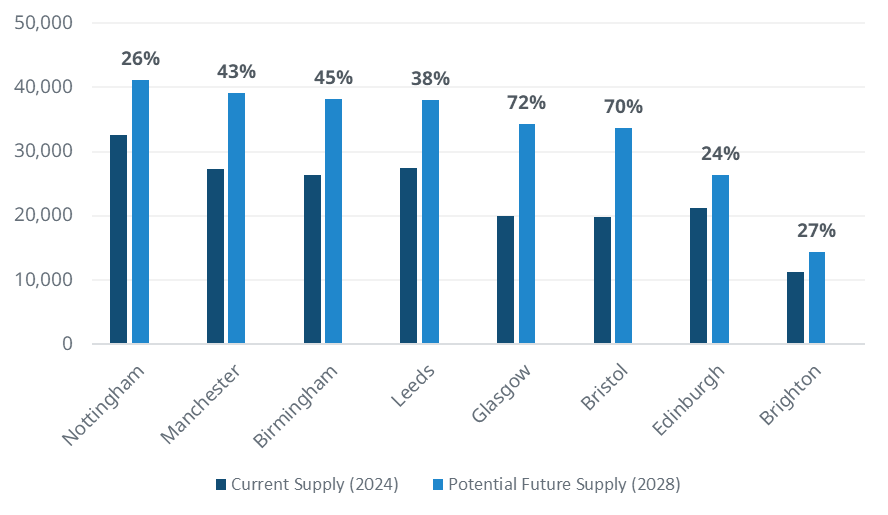

Looking beyond the national picture, the chart below illustrates how several key UK university cities could see significant increases in PBSA supply by 2028. Assuming a full delivery of the pipeline, Glasgow and Bristol stand out with the largest projected percentage growth, at roughly 72% and 70% respectively. By comparison, Manchester and Birmingham show potential expansions of over 40%, while Leeds is projected to add close to 38%. Even cities with more modest increases, such as Nottingham, Brighton, and Edinburgh, still highlight a steady upward trajectory.

Figure 2: City-by-City Growth Potential (Select Cities)

Source: StuRents, all relevant local authorities

Historic Deliveries

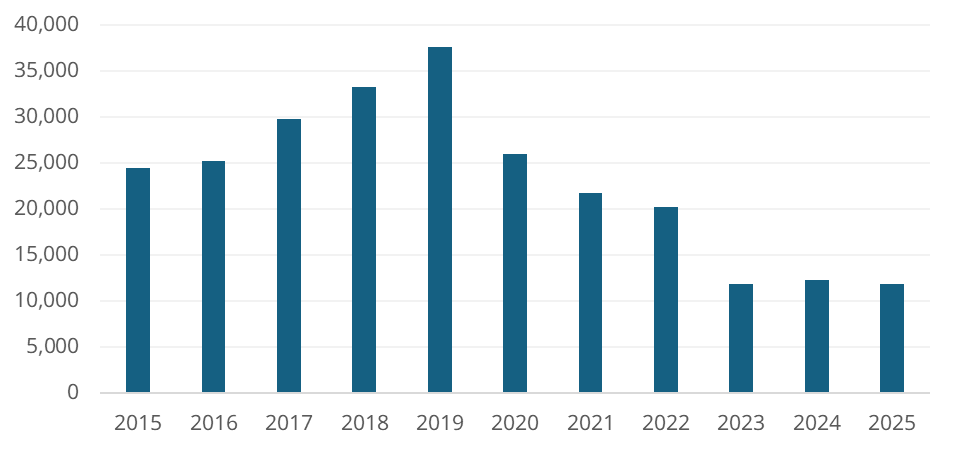

Over the past decade, the volume of beds delivered each year has varied considerably, reflecting the ebb and flow of construction completions and market sentiment. As shown in the chart above, annual additions have fluctuated from highs of almost 38,000 beds in 2019 to more subdued activity in recent years. For the upcoming 2025/26 academic cycle, we’ve already identified around 11,862 beds across the UK that are already being marketed. It’s worth noting that this figure will likely evolve as more schemes are completed in the run-up to the next academic intake.

It’s important to bear in mind that final delivery numbers can shift in the months ahead due to factors like construction schedules. However, this preliminary snapshot provides a useful indication of how the PBSA pipeline is shaping up for 2025 and underscores the slowdown in the number of beds being delivered.

Figure 3: PBSA and University Beds added by year

Source: StuRents

Beds added by city (2025-26)

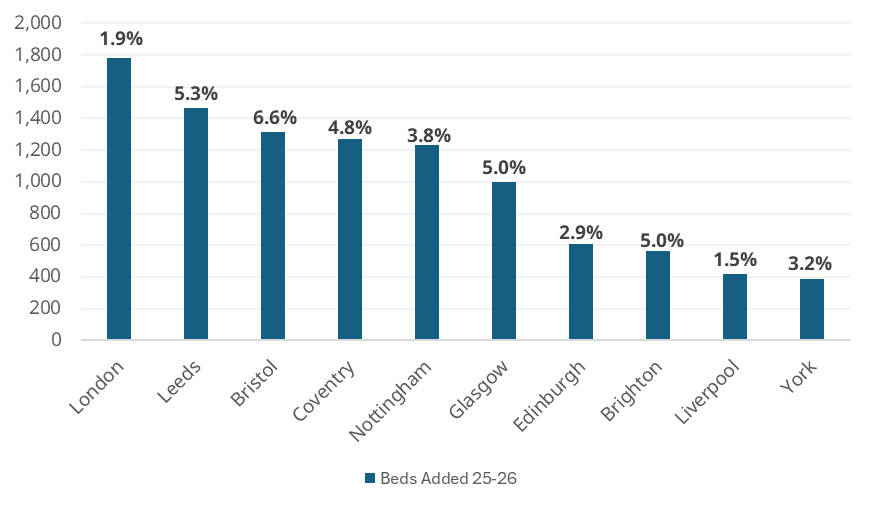

When we zoom in at the city level, we see that some markets are poised to receive more new PBSA beds than others in the 2025/26 academic year. In the chart below, which highlights the top 10 locations, London leads in absolute numbers with at least 1,779 new beds set to come online, though this represents a relatively modest year-on-year growth of 1.9% given its already expansive supply base. By contrast, Bristol’s 1,317 additional beds translate into a 6.6% hike in its total stock, while Leeds sees 1,466 new beds for a 5.3% increase.

Other standouts include Coventry, Nottingham, and Glasgow, each exceeding 1,000 new beds and displaying growth rates between 3.8% and 5%. Meanwhile, cities like Edinburgh and Brighton fall slightly lower in total bed additions but still see meaningful expansions in percentage terms relative to their overall supply.

Figure 4: PBSA Beds Added 2025-26 (Select Cities)

Source: StuRents

From national forecasts to city-specific expansions, it’s clear that interest in student accommodation will continue to result in more PBSA being delivered. While certain hubs such as Glasgow, Bristol, and Manchester appear poised to see the most significant percentage increases, even traditionally mature markets like London continue to expand. With new developments still in the pipeline and ever-evolving factors like construction costs, planning permissions, and shifting student demographics, the final shape of the market remains fluid. Nevertheless, the overall direction is unmistakably upward, indicating strong confidence from both investors and institutions. As we move closer to the 2025/26 academic year and beyond, the PBSA sector will likely remain a key focus for those seeking to gain exposure to a sector with positive headline fundamentals.

Share

Article by

Research Analyst at StuRents

Calum Martin is a research analyst in StuRents’ research division, StuRents Intelligence.