StuRents Q2-2025 Webinar Roundup

Image courtesy of Flickr

We recently hosted our Q2-2025 Webinar, where we presented the latest trends and insights from the sector, alongside a great guest presentation from Landmark Properties. We also had time to answer and discuss some questions from our audience. Here, we round up some of the key takeaways from the session and answer some of the questions we received.

Changing Dynamics

Source: Office for Students

Despite this Office for Students (OfS) data being an ‘early estimate’ of student numbers for the year, it is a good indication of how things are moving - historically mirroring the trends seen in HESA’s student numbers once released. The 2024 OfS data shows a lot of variance in overseas student recruitment, with cities such as Birmingham and Bristol continuing to grow year-on-year. This contrasts other Russell Group locations such as Leeds and Sheffield, who have seen their overseas numbers fall sharply.

PBSA Occupancy

Source: StuRents Occupancy Survey

Data from the StuRents Occupancy Survey is showing that, as of March, both cluster and studio bookings have declined year-on-year, with studios showing a more pronounced fall compared to 2024-25 levels. Clusters were down 9.0 percentage points YoY in March, with studios down by 13.4. These comparisons to the ‘post-Covid boom’ years are unflattering, however this year looks more in line with the era before that, suggesting booking velocity could be returning to the levels seen then.

Student Behaviour

Source: StuRents

The average viewed price for a Chinese student on StuRents.com is still well above that of a British student - £220 pppw vs £160 pppw for the 2025-26 academic year. However, while the average viewed price for British students continues to grow year-on-year (albeit slowly), the average for Chinese students has decreased by 1.2%, after a period of sustained growth.

Planning

Source: StuRents, all relevant councils

While the number of beds submitted for development nationally in the last 12 months stands at a significant 40k, the vast majority of those are concentrated in a few major cities. Glasgow, second only to London, has a pipeline more than twice the size of anywhere else, excluding the capital. While Glasgow has typically been seen as an undersupplied market, there’s potential for the supply vs demand scales to tip in the opposite direction over the coming years, if the majority of these planned beds are delivered.

Q&A

Why are Leeds and Sheffield’s OfS overseas numbers down so much?

The sharp decline in overseas students seen in the OfS data for Leeds and Sheffield can mostly be attributed to a decline in postgraduates. Universities in both of these cities rapidly increased their overseas postgraduate intake in recent years, with changes to the rules surrounding international student visas and an uncertain geopolitical environment being possible factors for the recent dips.

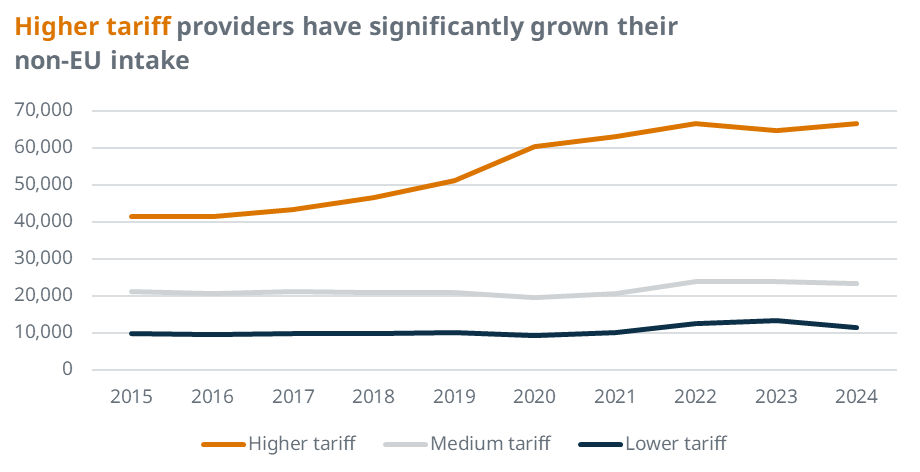

How do you feel about the prospects for low, medium, and high tariff markets?

Source: UCAS

The above two charts illustrate how demand for high, medium and low tariff HE providers varies by demographic. For non-EU students, the growing demand for high tariff over others is clear, with intake for medium and low tariff providers stagnating. The picture for British students is less clear, with medium tariff providers growing long-term alongside the higher tariff ones.

The Occupancy Survey charts show data up to March, are you seeing a pick-up in April?

As previewed in our June newsletter (which you can sign up to here), booking velocity has picked up slightly month-on-month in April, which could indicate the beginnings of a market recovery. Although whether the market is slow or genuinely low this year still remains to be seen.

Participants in our Occupancy Survey already have access to data for April - join today to receive exclusive insights and benchmark your performance against a combined portfolio of 170,000+ beds.

We will also be releasing an updated Occupancy Report for 2025 very soon - watch this space!

For more information about our proprietary, highly granular data covering UK student accommodation contact the StuRents Research team today. Or book a demo of our Data Portal to find out how you can have up-to-the-minute university housing insights at your fingertips.

Watch the full webinar recording here.

Share

Article by

Research Analyst at StuRents

Sam Gillespie is a research analyst in StuRents’ research division, StuRents Intelligence.