Student Market Demand Assessment: Nottingham & Beyond | StuRents Summit Update

We recently hosted the 2025 StuRents Summit at The Pelligon in Canary Wharf, bringing together over 200 professionals from operators, owners, investors and marketers. We’ve summarised some of the highlights from presentations and panel discussions, giving insights, expectations and predictions for this year and beyond in the student sector.

PBSA - Market fundamentals and leasing velocity

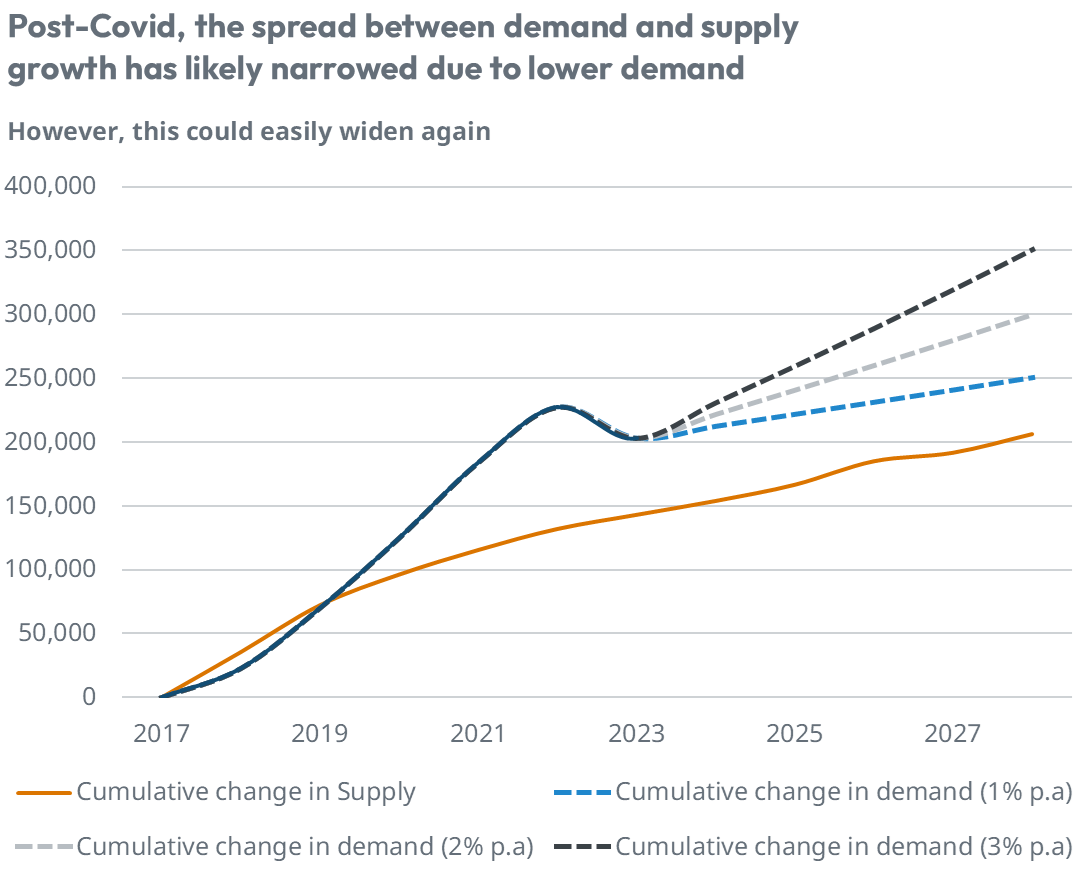

Nationally, the Purpose Build Student Accommodation (PBSA) supply and demand spread looks to be narrowing as the post-Covid recruitment boom has settled in the last two years, lowering projected student demand. Data from the StuRents Occupancy Survey also shows some potential difficulties at a national level, with leasing velocity for studios and clusters down 13.8 and 9.6 percentage points respectively.

Figure 1: National Projected Supply vs Demand

Source: StuRents Intelligence

Note: Pipeline assumes 40% of beds are delivered and 20% of returning British students choose PBSA, excludes London

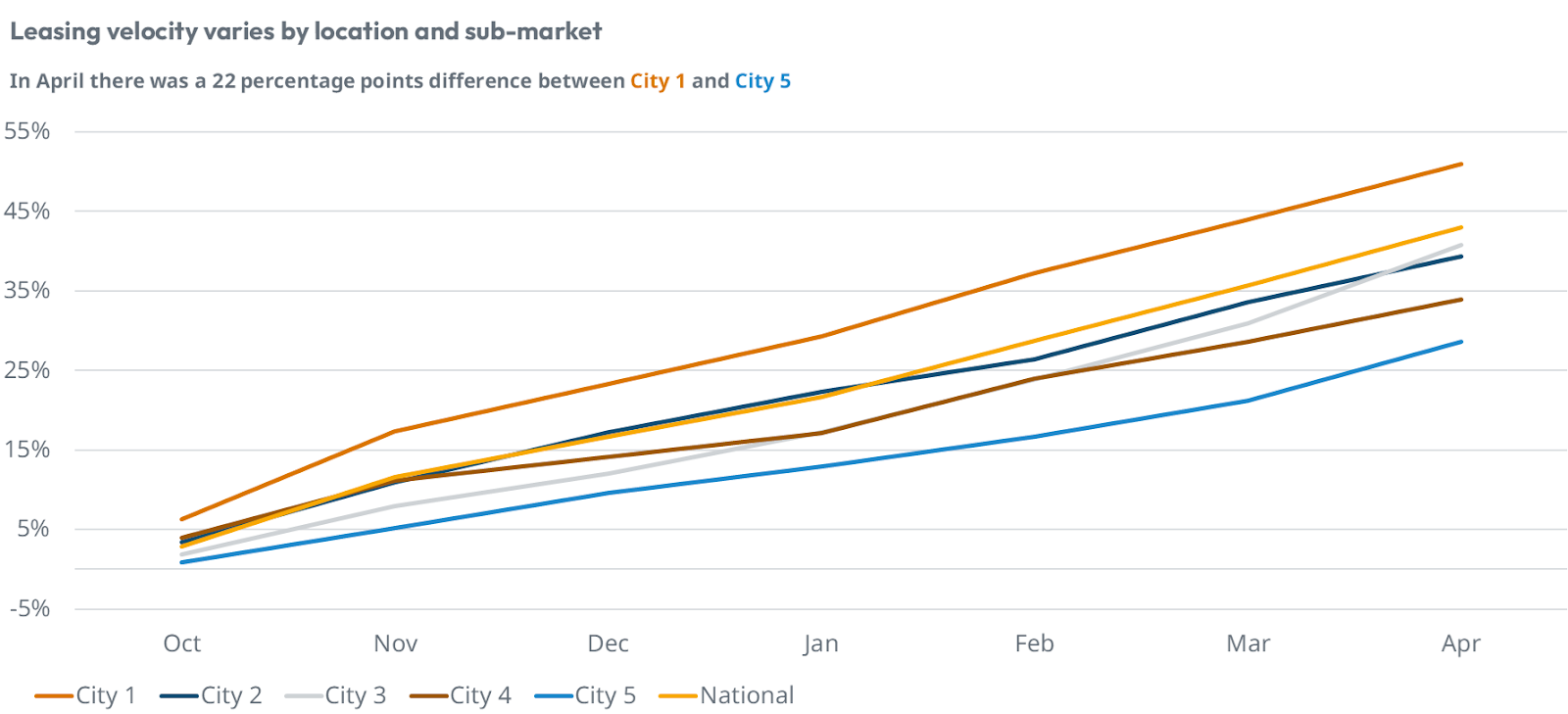

As with much sector data, national trends hide significant city and individual market variations; for some cities in our occupancy survey there is up to a 22 percentage point difference in leasing velocity as of April. In the panel discussion, points were raised that occupancy may be settling at a ‘new normal’ after post-Covid over-recruitment and that current leasing velocity aligns more closely with the 2021/22 and 2022/23 academic years. It’s worth noting that if demand growth is more than 2% per annum, the spread between supply and demand could widen again, which in turn could improve leasing velocity.

Figure 2: Leasing velocity of 5 example cities and National data

Source: StuRents Occupancy Survey

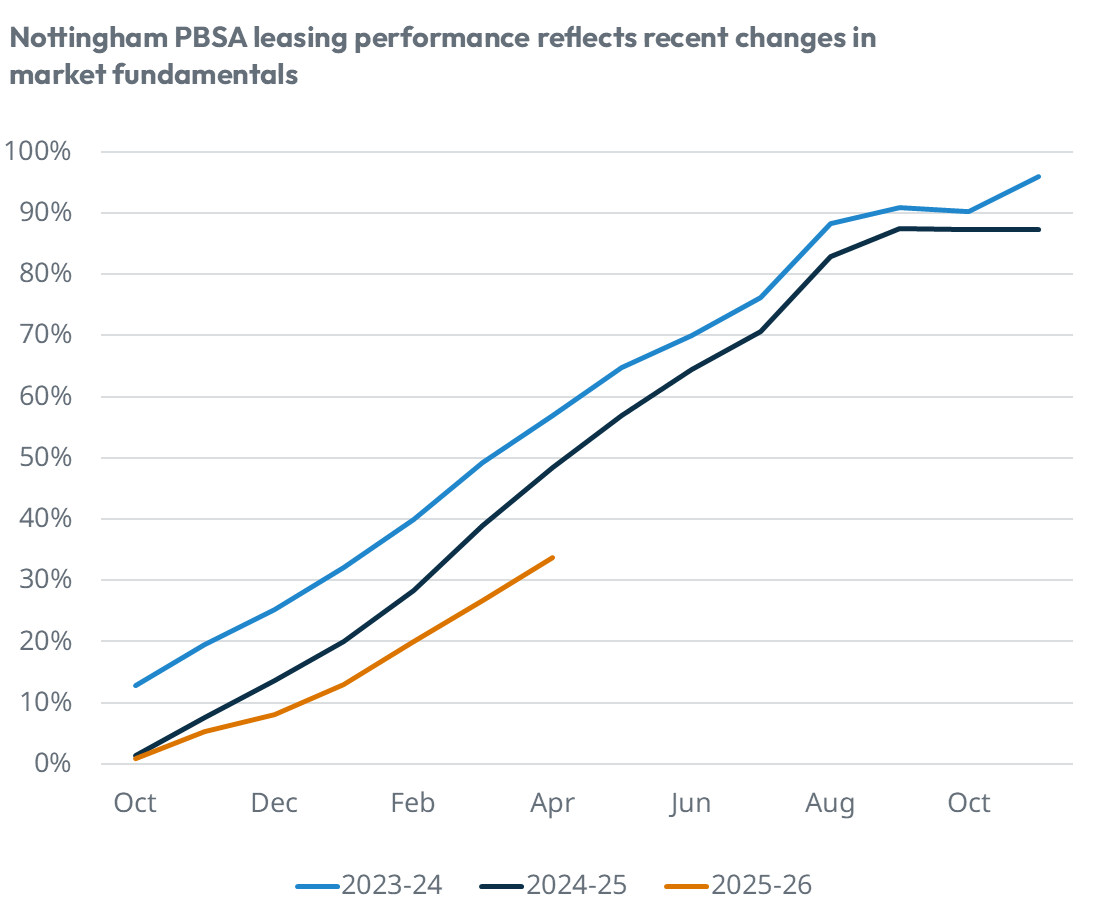

Looking in more detail at Nottingham, projected supply growth is unlikely to be matched by projected demand which indicates a less positive market outlook. This is supported by occupancy data where leasing velocity is slower and could end up down overall year-on-year (YoY). Similarly, rents in Nottingham are trending down and could be showing early signs of discounting in an attempt to fill beds. In our panel discussion, Nottingham was highlighted as a location where the conversion rate is down YoY.

Figure 3: Leasing velocity for Nottingham

Source: StuRents Occupancy Survey

Leicester, however, shows more positive trends. Leasing velocity is in line with the past two years and is currently outperforming the national market; the expectation is that the overall leasing trend will be consistent with previous years. While recruitment volatility has affected the market up to 2023, a demand growth of 2% per annum could keep the market in balance - an expectation reinforced by leasing velocity. Similarly, rents are trending up, indicating a stronger market overall.

The panel noted that stakeholders should consider asset stabilisation time when comparing occupancy to the wider market, and that it can vary by microlocation. They also noted that rebookers and student retention was important to filling PBSA and driving occupancy, with incentives, university advice and trust all part of a complex decision making process for students and parents - and not always in alignment.

HMO - Student preferences and the Renters’ Rights Bill

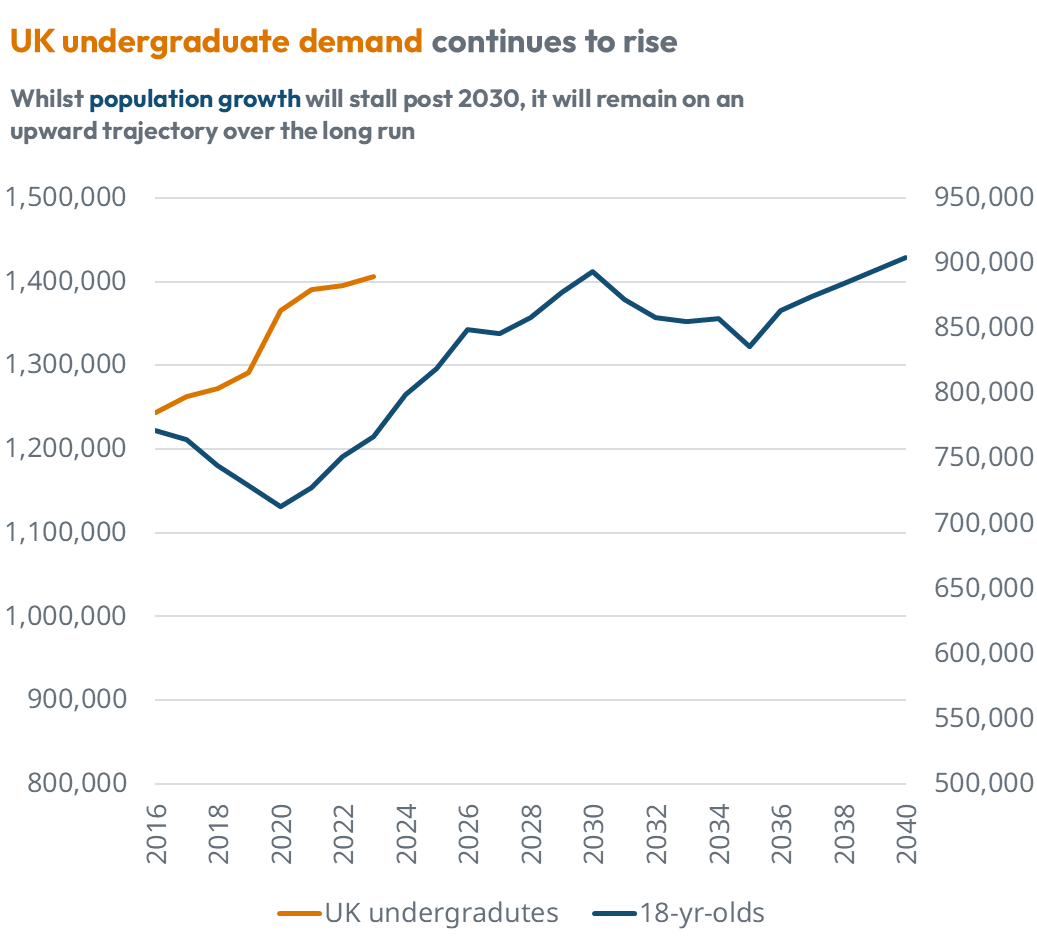

Outside of PBSA, Houses in Multiple Occupation (HMO) demand is expected to grow. Domestic students still have a clear preference for HMOs at 77% of executed tenancies (from Concurrent), - a preference noted by other panellists. UK undergraduates continue to rise; while the UK 18-year-old population is predicted to stall and decline in the 2030-2037 period, growth will be positive long term.

Figure 4: UK undergraduate demand and population growth of UK 18 year olds

Source: StuRents Intelligence, UCAS

Comparing domestic students with Chinese students, who make up the second largest international student population (HESA, 2023/24), less than 20% of Chinese students choose HMO over other accommodation options (executed tenancy data, Concurrent). There are many factors that may play a role in this, including cost, availability and rite of passage for domestic students moving into HMO - however there is a clear price sensitivity between demographics. Chinese students, on average, executed HMO tenancies at greater than £220 per person per week (pppw) compared to less than £160pppw for British students. Thus, international students with higher budgets are important to consider for HMO properties on the upper end of the price spectrum.

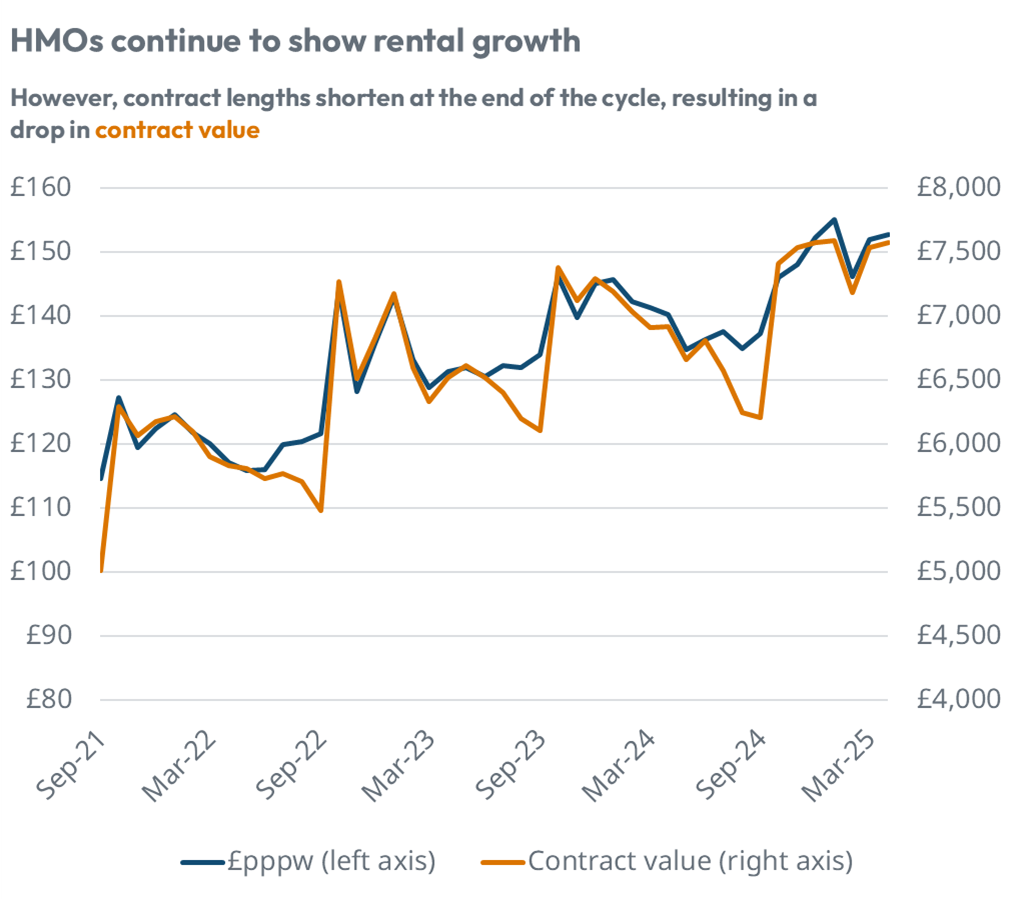

HMO rents continue to rise long term. However, contract lengths shorten at the end of each academic cycle, dropping the contract value at those times. As we outlined recently, tenancy length is an important consideration to understand total contract value and revenue change over time - rental figures may not give an accurate picture of the YoY market changes. HMO properties remain a strong asset class, with the discussion noting that they offer a cost-effective option for students and a resilient asset for owners and investors due to their flexibility and alternative use value. The granular and distributed nature of properties makes scaling a challenge - but data-driven decision making can offset some of the risks.

Figure 5: Weekly rental price (£pppw) and contract value over time

Source: StuRents Intelligence, Concurrent.co.uk

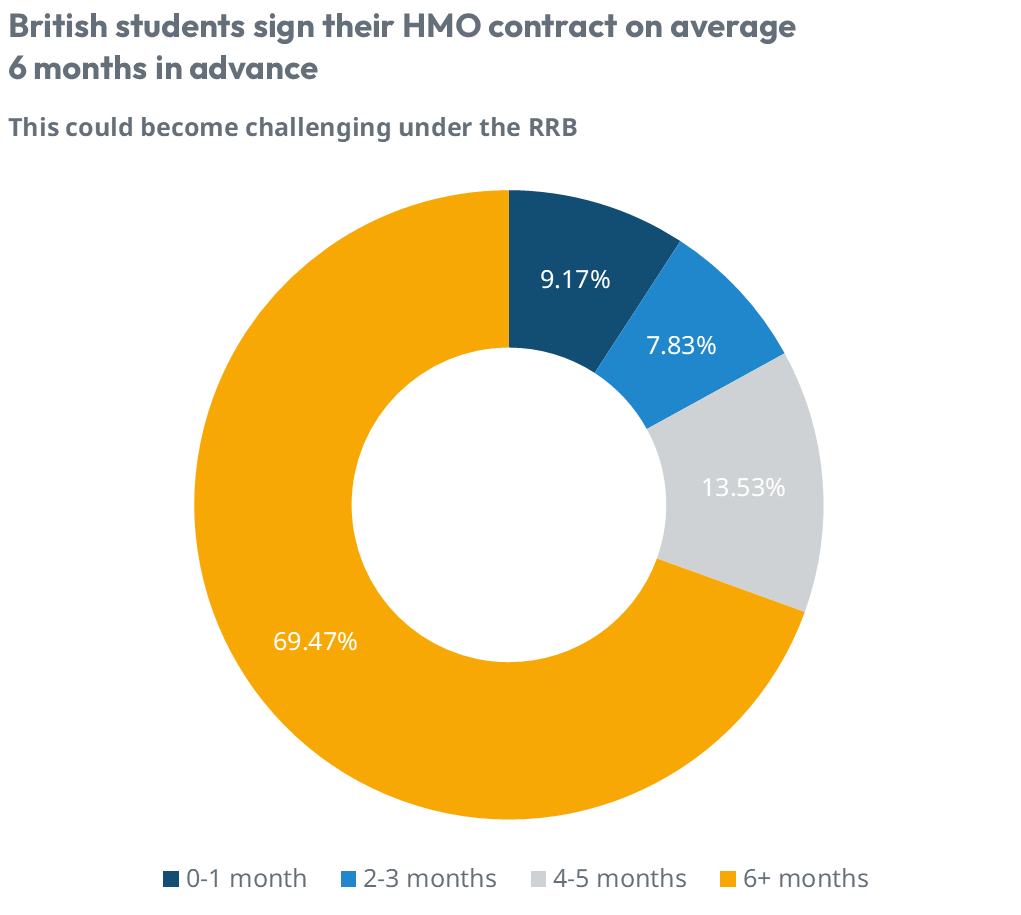

Much discussion recently has been around the Renters’ Rights Bill (RRB), with the PBSA sector hopeful for exemptions. There could be significant effects on HMOs, however, where our signed tenancy data from Concurrent shows that the majority (70%) of British students, on average, sign their contracts 6 months or more in advance - which will become challenging post RRB. This could present an opportunity for the PBSA market, appealing to students who are looking to secure their university accommodation as early as possible.

Figure 6: Breakdown of when students are signing their contracts relative to start date

Source: Source: StuRents Intelligence, Concurrent.co.uk

Note: Min contract length of 30 weeks

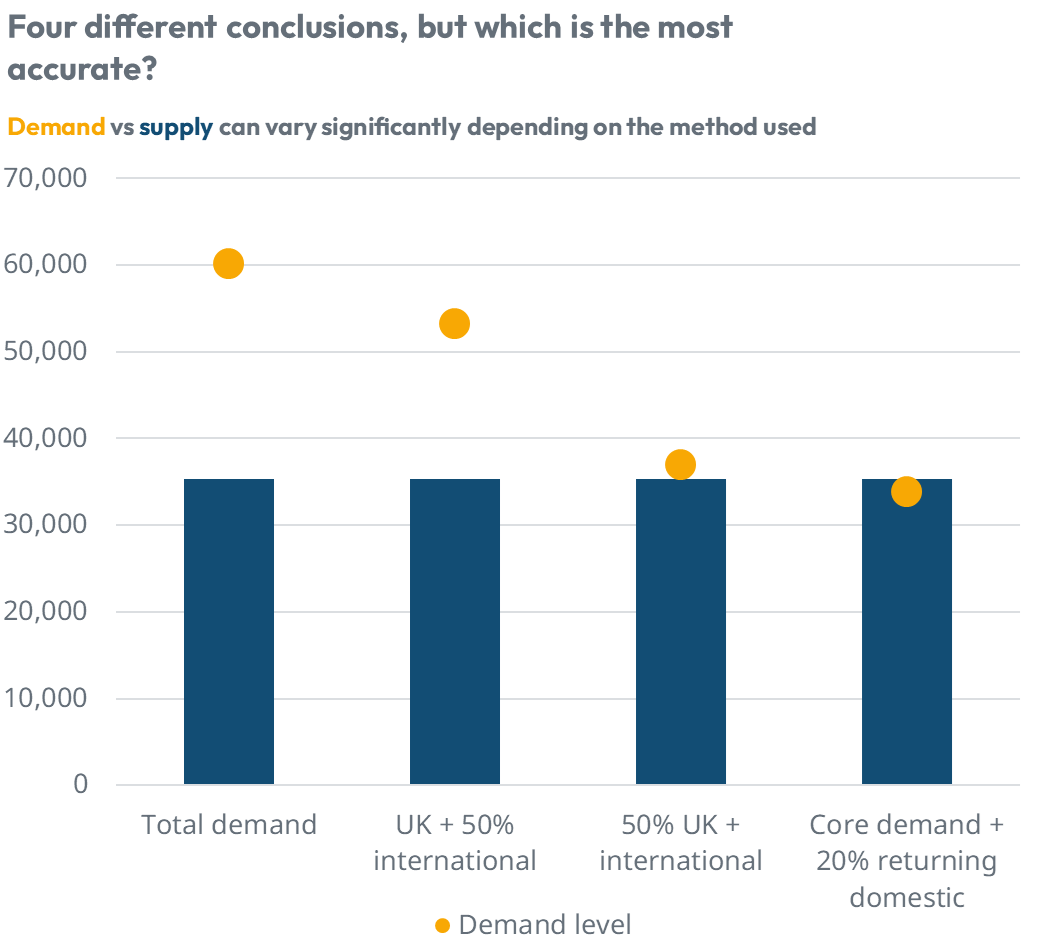

At the foundation of all the analysis is data, where quality and use still has wide variations across the sector, creating challenges in accurately determining market fundamentals and setting projections or expectations. Taking one example location, varying assumptions in demand figures can create wildly different market outlooks. We believe that more cautious assumptions on demand provides a better representation of supply and demand and fairly represents the effect of HMO and student preferences in the market - which is overall supported additionally by what we’re seeing in our Occupancy Survey data. Our panel discussion also noted that data communication and sharing within businesses is also critical to maximise its benefit, and that the human element of the sector is equally important to maintain.

Figure 7: Supply vs demand analysis for differing demand assumptions

Source: StuRents Intelligence

Note: Assumes no growth in demand since 2023

PBSA, Build-to-Rent (BTR) and Co-living - how sectors are converging

BTR was addressed in our second panel session, covering what differentiates the offer of this and co-living from PBSA and how this is affecting where students choose to live. The panel commented that PBSA is a student-centric and tailored offer, and that professionally managed brands in a mature sector can draw students in with an experience and amenities not always readily available in BTR schemes. Similarly, BTR schemes are geared towards young professionals and families, and their needs.

Looking at pricing, some BTR units - particularly larger units with 2 or 3 beds - are comparable with PBSA en-suite rooms and studios. This makes them an attractive option, particularly for anyone with higher budgets (such as international students), those looking for accommodation with pets, or to live with a partner. It was noted that student percentages in some BTR schemes are dropping, which may be beneficial for operators who are looking to avoid annual re-leasing associated with students renting for the academic year. Additionally, panellists commented that a higher proportion of young professionals and families are likely to help stabilise assets in the longer term.

Ultimately, BTR poses a challenge to the PBSA sector to focus on what differentiates their offer, what residents actually want from their accommodation for services and amenities, and how this provides the best value to new or rebooking students.

The investor landscape and future forecasts

The next panel took a look at the student sector through an investor lens. The UK student sector shows strong long-term fundamentals, but panellists highlighted that legislation and macroeconomic uncertainty is putting increasing pressure on the sector.

UK universities remain a top destination for international students with both Indian and Chinese demand remaining strong; while there is some shift in priorities towards value for money, international students - particularly from China - are still only attracted to top universities, with prestige a crucial factor in studying abroad. Therefore, interest in these locations remains high.

As seen earlier, the UK student sector is undersupplied on the whole - as discussion moved on to regulation, it was noted that increasingly complex planning processes and additional regulation are compounding problems in this area. The cost of new build PBSA is high due to rising construction costs, with rents needing to be over £200pppw for viability - again, this locks a significant portion of the domestic market out of this new stock due to affordability constraints, and thus mainly targets international students.

The effect of this is increasing interest in refurbishment, where resulting rooms can be delivered at costs much closer to the average budget of a British student - but questions around topics such as long-term sustainability, and increasing costs, pose constant challenges. It was highlighted that rent controls, where implemented, may reduce willingness to invest in the sector with the number of schemes in planning or construction dropping.

Investors remain committed to the student sector but are becoming increasingly selective about location, taking into consideration university performance and financial outlook. Appetite for alternative assets - including BTR and co-living - is growing, particularly to supplement PBSA portfolios in increasingly challenging markets. The panel noted that there may be opportunities for BTR collaborations with universities, to provide students with accommodation.

Overall, our panels highlighted that there is still a lot of opportunity in the sector; while government intervention and macroeconomic shifts pose risks and challenges, data and trends support long-term optimism. Leveraging available data is increasingly critical to inform medium- and long-term strategy, provide safe and affordable accommodation, and maintain investor confidence.

For more information about our proprietary, highly granular data covering UK student accommodation contact the StuRents Research team today. Book a demo of our Data Portal to find out how you can have up-to-the-minute university housing insights at your fingertips, or get in touch with us about our Occupancy Survey.

Share

Article by

Research Analyst at StuRents

David Reader is a research analyst in StuRents’ research division, StuRents Intelligence.