Converging supply in a maturing student accommodation market

Image courtesy of Flickr

Converging supply in a maturing student accommodation market

As the sector matures, the depth and quality of information available continues to grow. However, an area which has historically been a blind spot for the sector and still remains a challenge for some, is understanding what impact alternative asset classes are having on demand for PBSA.

Houses of multiple occupancy (HMOs)

StuRents has been listing hundreds of thousands of HMO beds for many years, ensuring we have a unique perspective on the supply of off-street housing, its location, make-up, price and the level of demand for this accommodation type.

With the HMO sector remaining hugely fragmented but representing a significant proportion of supply, we have long advocated for stakeholders to better understand this accommodation type to ensure more accurate analysis of supply and demand.

Of course, the Renters’ Rights Act could shape the market in the years to come. However, the exact implications are still unclear and could take some time to play out. Moreover, cost of living challenges remain as acute as ever, and with a lower entry price point, as well as the associated rite of passage, HMOs will remain the preferred choice for a material section of the market. This will ensure HMOs remain as important as ever when assessing existing levels of student accommodation.

Build to Rent (BTR)

What has changed in more recent years is the rise of BTR. The build-to-rent market is an example of an asset class that has somewhat taken the student sector by surprise. Leeds is the most commonly referenced example due to the substantial growth in supply recorded in recent years, which has dented demand for PBSA.

While BTR providers and investors will want to reduce their exposure to this tenant type over the long-term, which could result in a diminishing impact on PBSA over time, it can contribute to short-term occupancy challenges for the wider student market.

However, there remains a persistent challenge for the sector. How is BTR being factored into supply vs demand analysis, and can stakeholders be more forensic in their approach to ensure markets are fully understood?

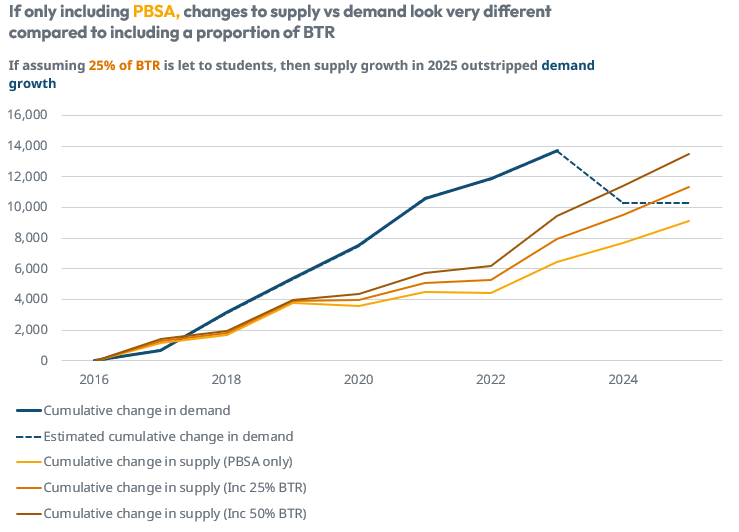

Let’s consider the supply vs demand analysis in Leeds, as represented below.

This analysis tracks the cumulative change in demand for accommodation over time, versus the change in supply based on a variety of assumptions, to understand whether a market is improving or deteriorating.

Starting with the analysis, inclusive of just PBSA. With demand in Leeds falling in more recent years, the spread between demand and supply growth has narrowed, resulting in tougher market conditions compared to 2022 and 2023, when the spread was at its widest.

We can then overlay BTR supply based on either a 25% or 50% uptake rate from students. Even at the more conservative 25% figure, the outlook does materially shift, with the analysis now suggesting that cumulative supply growth has outstripped demand growth, as represented by the orange line crossing above the navy line. This corresponds to the tougher market the city has recorded and, therefore, lower expectations related to occupancy and rental growth.

While it is possible to incorporate additional asset classes into supply vs demand analysis, it’s not without its challenges.

For example, within the sector, there is a significant spread in exposure between BTR and co-living operators, with some promoting hard student caps and others being almost 100% let to students. As such, depending on the assumptions being applied, the output can vary materially, as represented above.

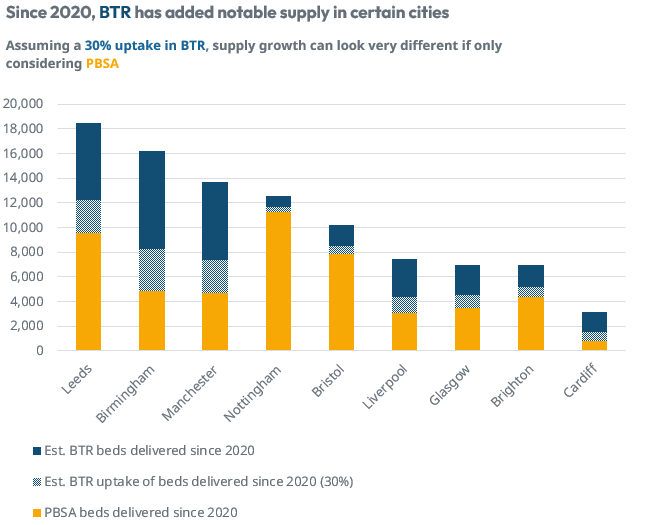

Further analysis of the growth in supply can also highlight the availability of more modern stock within a location. For example, the chart below depicts the number of new beds delivered since 2020 across a variety of markets. This analysis shows:

1. The number of new PBSA beds added

2. The estimated number of BTR beds added - assuming a 30% uptake by students

3. Total supply growth, inclusive of PBSA and all BTR.

This highlights that in a market such as Birmingham, where ~4.8k PBSA beds have been added since 2020, once adjusted to take into account a proportion of BTR beds, this can increase to almost 8k.

Similarly, while growth in absolute terms in Cardiff has been low, with fewer than 900 PBSA beds added since 2020, this figure nearly doubles once adjusted to account for 30% of BTR beds added over the same period.

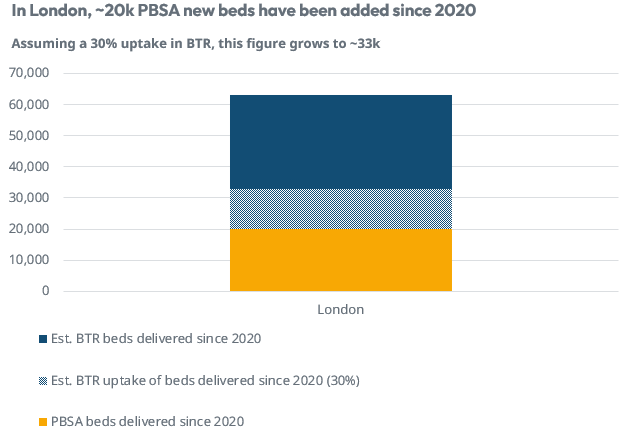

London shows a similar pattern. With supply growth since 2020 rising to almost 33k beds, if including a proportion of BTR.

Requests from operators of BTR and Co-Living to advertise on student-dedicated marketing platforms indicate that, at least in the short term, BTR and Co-Living’s exposure to students will remain an important consideration.

Therefore, those stakeholders able to access quality data across the entire rental spectrum will be better positioned to understand the supply vs demand dynamics in a given location in much more detail, leading to better informed decisions and a lower risk of misallocating capital to markets where perhaps the fundamentals are misaligned with expectations.

For up-to-date data to support rent setting, underwriting, and broader industry benchmarking, the StuRents Data Portal provides users with instant access to sector-leading data.

Share

Article by

Head of Research at StuRents

Richard leads the StuRents research team, providing proprietary, platform-driven insights to help stakeholders make better-informed decisions about the market.