Interest in UK student HMOs continues to grow

Image courtesy of Flickr

HMO Demand Fundamentals

With the recent announcement regarding Brookfield’s foray into UK HMOs, as well as the notable commitments from GCM Grosvenor, the sector has seen an increase in institutional interest in recent months.

While much of the sector commentary focuses on PBSA, HMOs remain a vital segment and equate to roughly 50% of all available supply. Looking at the headline demand trends, it's clear to see why there is growing interest.

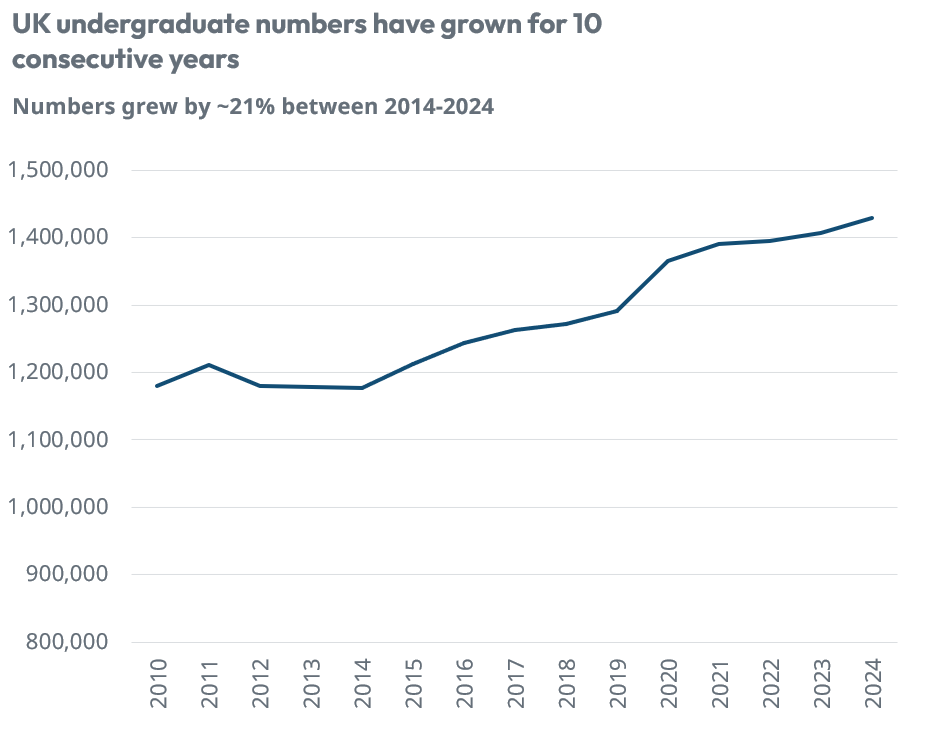

As of 2024-25, ~65% of the total full-time student population consisted of UK undergraduates, with this cohort reporting 10 consecutive years of growth.

On the supply side, the slowdown in the delivery of PBSA is well-reported, but Article 4 directions, implemented at a local level, place significant barriers to increasing HMO supply too. Furthermore, with the 18-year-old population expected to grow up to 2030, there are positive tailwinds in the medium term.

Sector Naunces

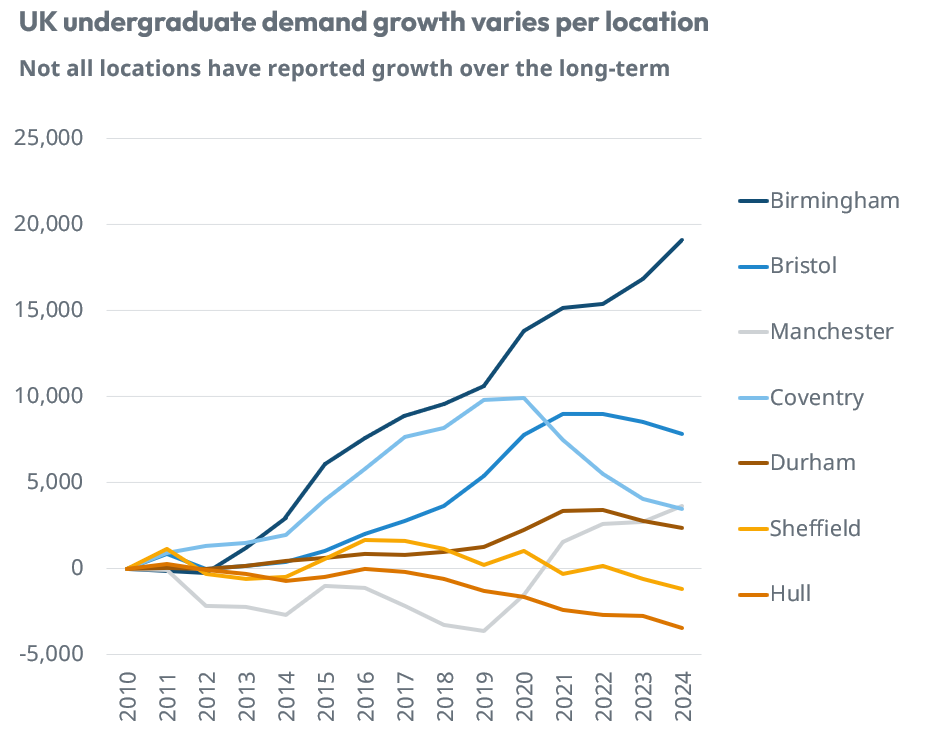

Of course, national trends don't do justice to the nuanced nature of the market and as highlighted below, changes in UK undergraduate numbers vary significantly by location.

For example, in 2024, there were ~19k additional UK undergraduates in Birmingham, compared to 2010. Other markets, such as Coventry, were reporting strong growth up until 2020, but have since seen numbers decline by ~6k. Sheffield and Hull have struggled with growth, and reported numbers ~1.2k and 3.4k lower in 2024 compared to 2010.

Therefore, it is not only important to understand localised historical trends, but also how these may change going forward and the potential positive or negative impact on demand for HMOs.

British Appeal

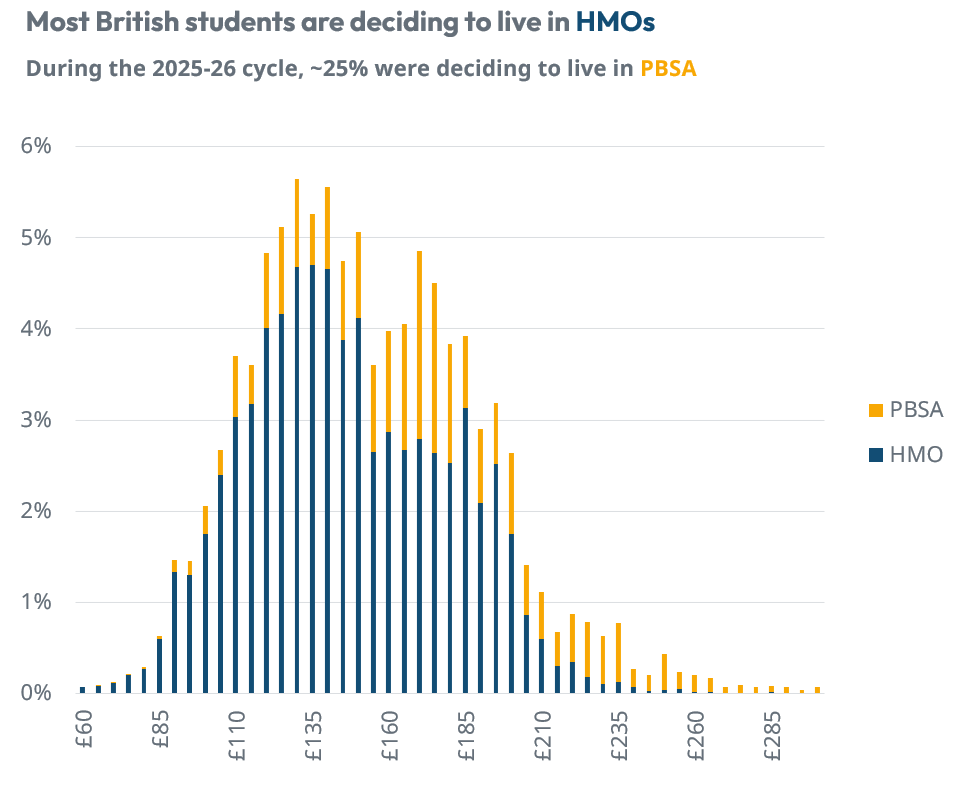

Of course, HMOs are not the only accommodation type available to UK students. However, our own proprietary data based on executed contracts highlights their continued appeal. In the 2025-26 letting cycle, around 75% of agreements signed by British students were done so in HMOs, with the balance deciding to live in PBSA.

This data can also be used to understand the demand pool by price, with more than 73% of British students deciding to reside in accommodation priced between £100-£180pppw. Only 12% of this demographic was prepared to pay £200pppw or more, highlighting the comparatively small demand pool at this price point, at least for British students.

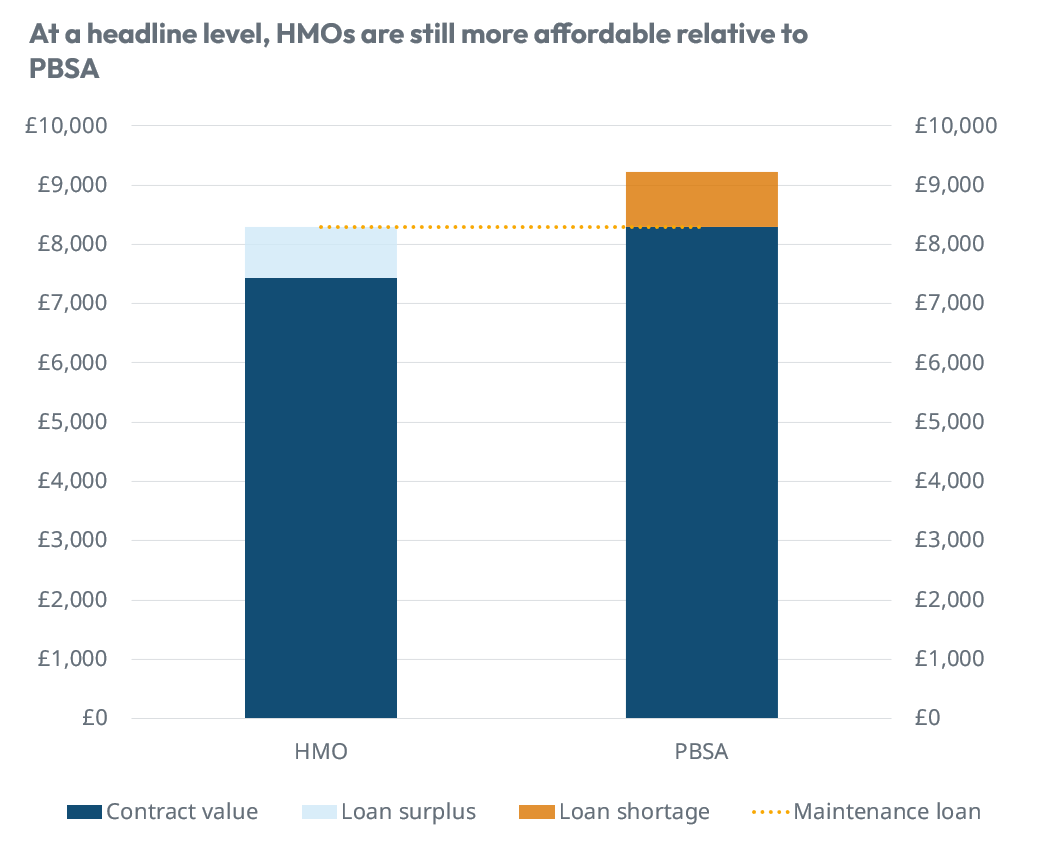

While cultural differences and the familiarity of the HMO product will be important drivers of demand, affordability remains a key consideration. Many commentators in the sector typically refer to affordability in reference to the maximum maintenance loan available to students. However, the vast majority do not receive this, and so it’s not reflective of the cost pressures most students face. This is something we highlighted in more detail in our 2025 UK Student Accommodation Report.

Adjusting the available maintenance loan based on a total family income of £40k p.a. can be useful in understanding the cost difference between accommodation types. For example, on this basis, a British student living in an average HMO will be left with a headline yearly surplus of ~£850. In comparison, those living in PBSA will face a shortage of more than £900. Psychologically, this perceived shortage compared to a surplus will be too large a barrier to overcome for many, while the wider cost-of-living pressures faced by many families will make it more difficult for some to offer additional financial support.

HMO Outlook

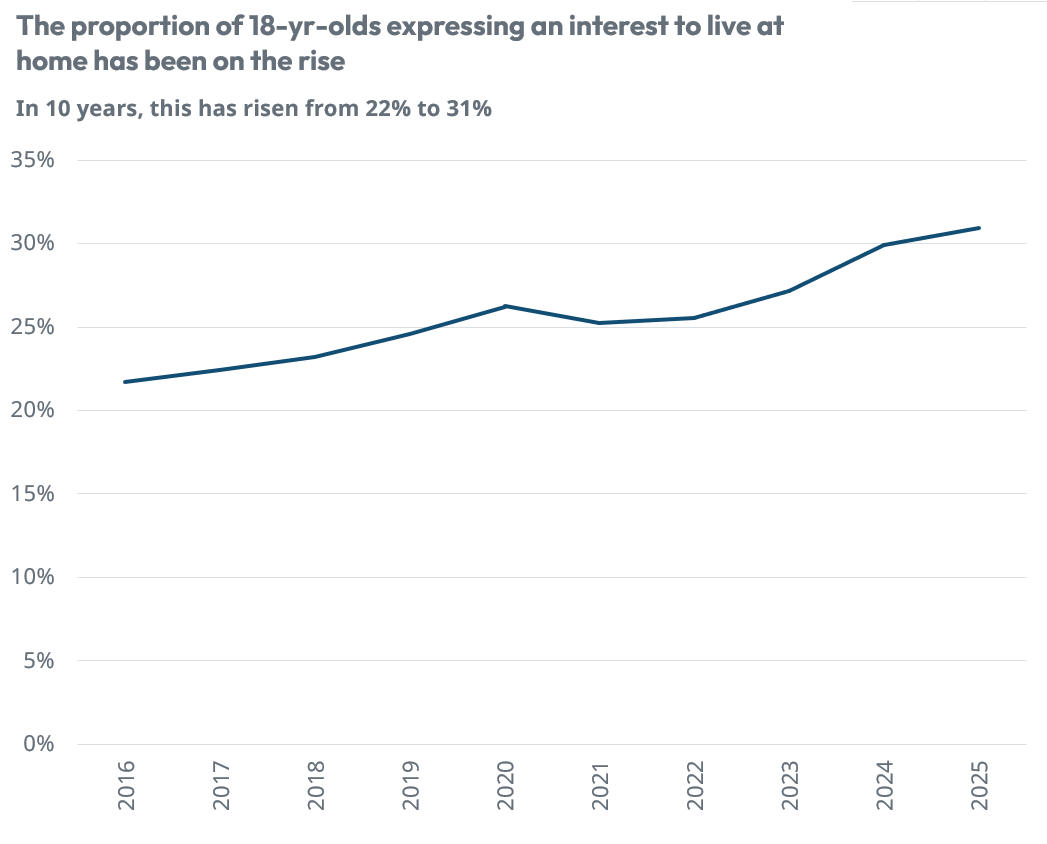

While there are many factors which make HMOs a compelling choice, they are not without their risks. The exact impact of the Renters’ Rights Act is still unknown at this stage, while a growing number of students, in the face of higher costs, are deciding to live at home.

Data released for the first time this year by UCAS indicates that the proportion of 18-year-olds intending to live at home has risen to 31%, up by more than 9 percentage points in a decade. If this trend continues, it’s likely to offset some of the expected demand growth, albeit local variations will again be critical in understanding the impact on a particular stock.

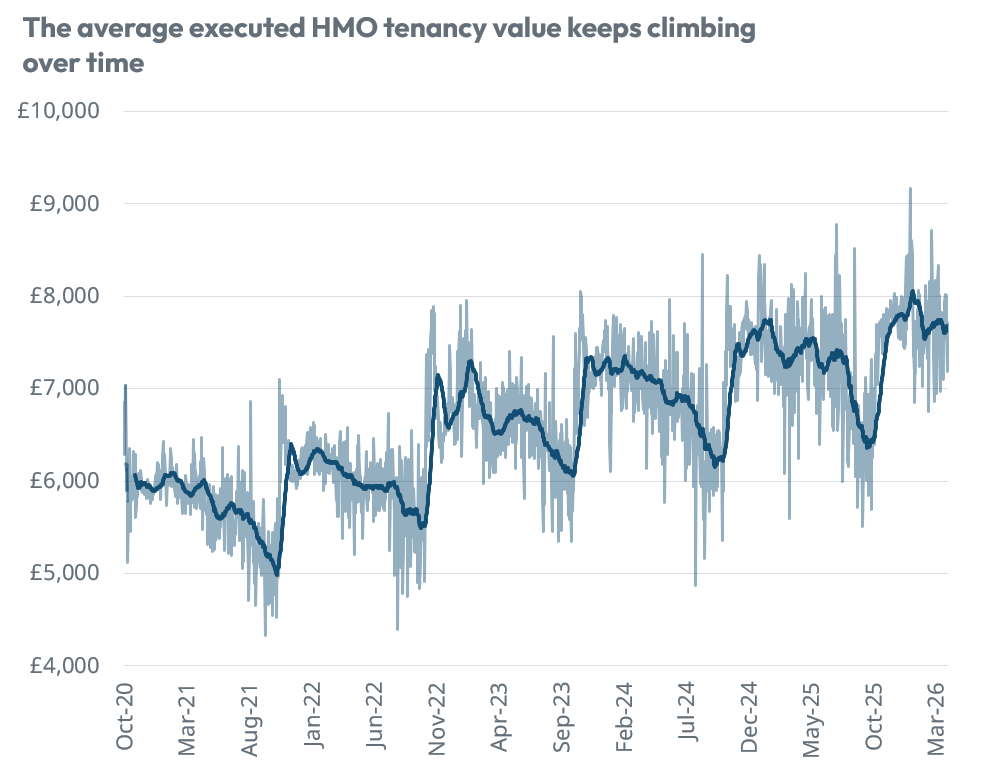

For those investors taking a long-term view, continued growth in rents and contract value will be an attractive historical trend. With limited supply growth and expected growth in students, there will be instances where this trend is expected to continue, providing opportunities for savvy investors to benefit from higher rents in markets where price elasticity is more forgiving.

The UK student accommodation market is one which contains significant nuances and the HMO market is no different. While there are many positive macro-related trends, which provide a great bull case for further investment, the sector is not risk-free, with affordability likely to be the defining trend over the next 5 years.

For up-to-date data to support rent setting, underwriting, and broader industry benchmarking, the StuRents Data Portal provides users with instant access to sector-leading data.

Share

Article by

Head of Research at StuRents

Richard leads the StuRents research team, providing proprietary, platform-driven insights to help stakeholders make better-informed decisions about the market.