Occupancy Update - March 2026

Image courtesy of Flickr

We’re now six months into the 2026-27 PBSA leasing cycle, and this piece explores how the cycle is progressing across the UK market, analysing booking trends, year-on-year performance, and seasonal patterns by bed type. It also reflects an expanded dataset – with Bristol, London, and Oxford recently added – meaning the survey now captures around 50% of the private PBSA direct-let market, offering the most comprehensive view of current market dynamics available.

StuRents Occupancy Survey includes private PBSA direct-let bookings only. University halls and private beds on nomination agreements are excluded.

Source: StuRents Occupancy Survey

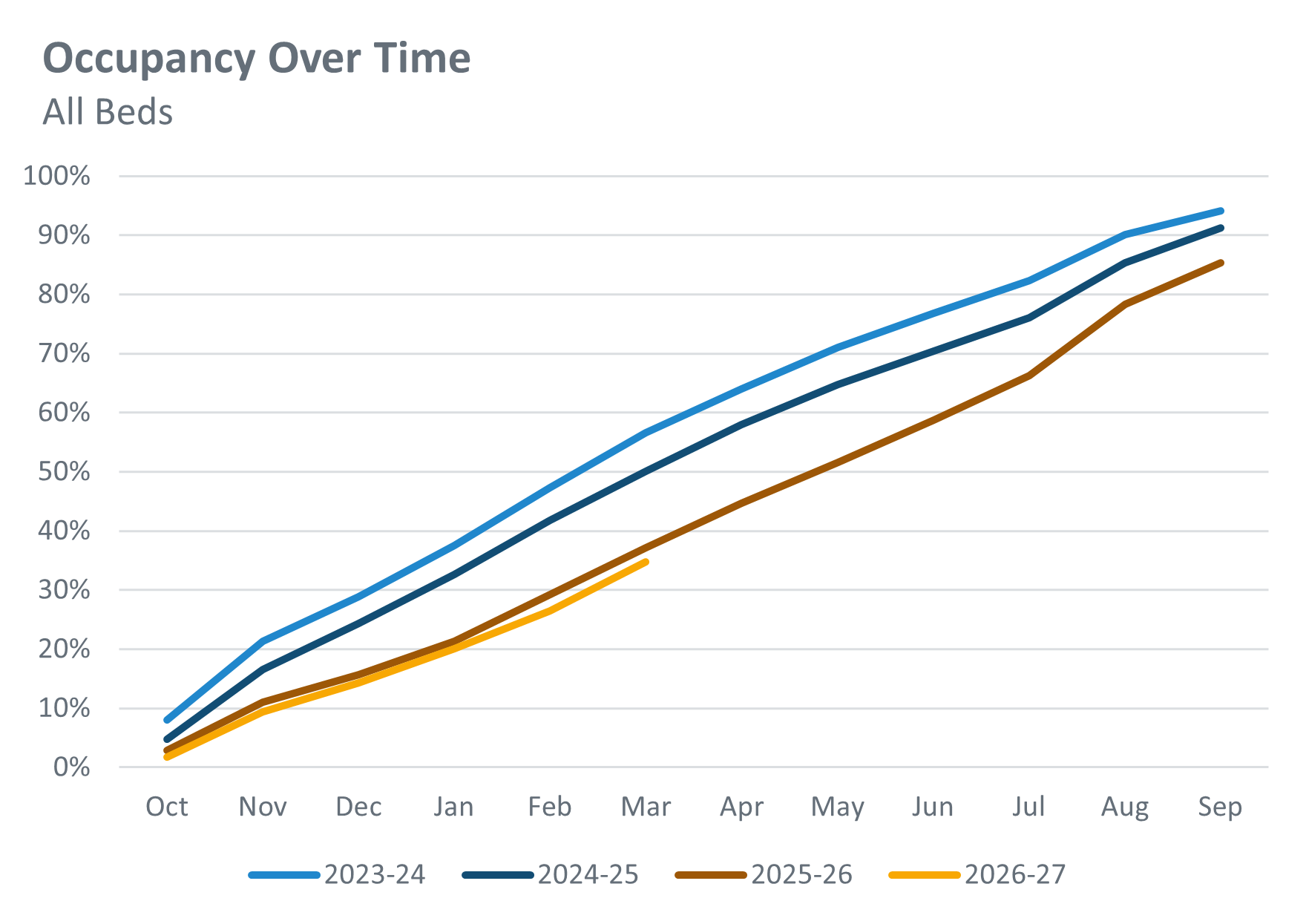

The above chart is showing how 26-27 leasing velocity has been broadly in line with that of 25-26, which itself consistently lagged behind that of the two previous years. Across all bed types in all 28 locations we cover, average occupancy for 26-27 stood at 34.8% as of the end of March. This represents a 2.4 percentage point drop year-on-year (YoY).

Source: StuRents Occupancy Survey

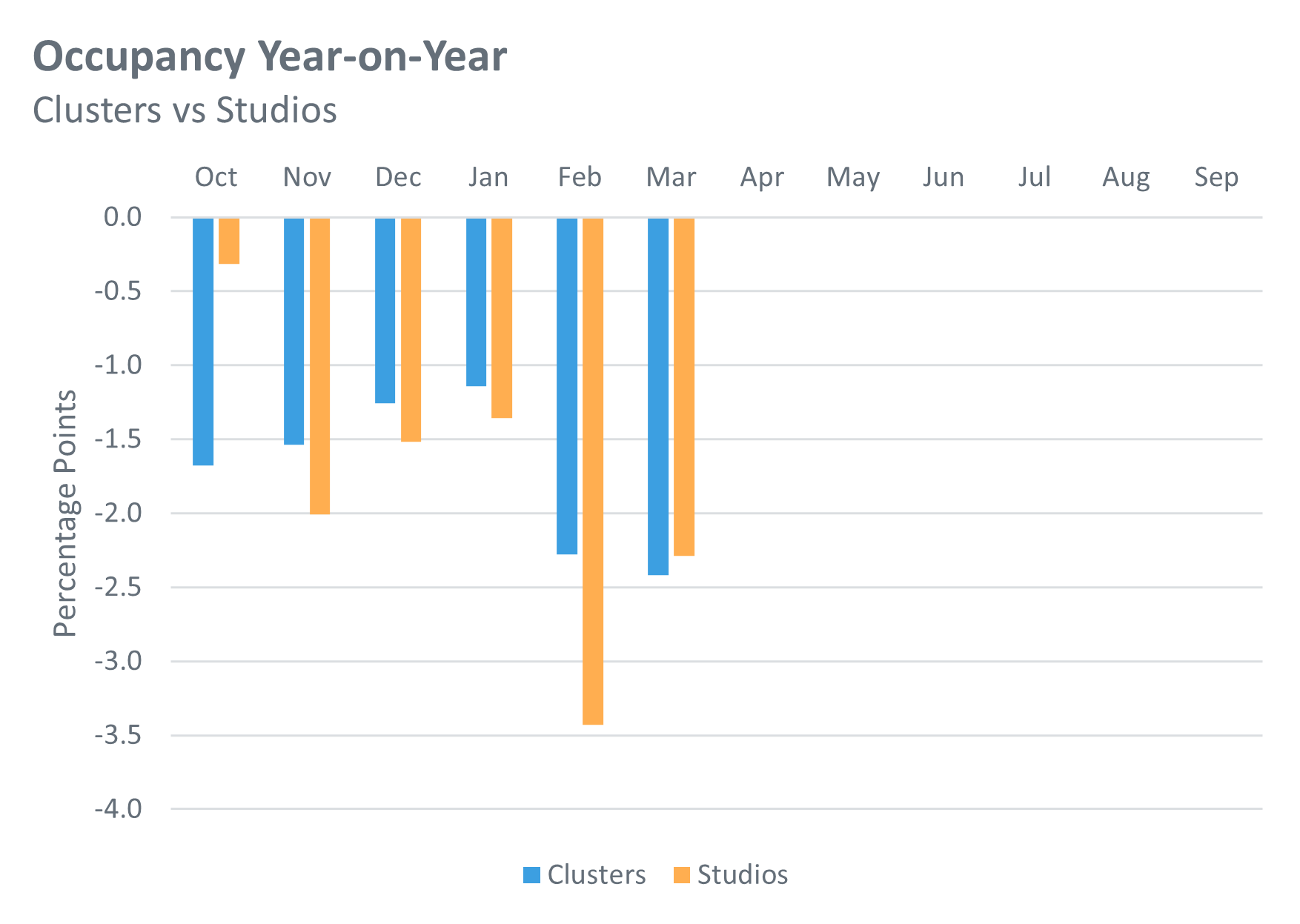

The above is showing how the YoY gap in bookings has changed throughout the cycle so far, for both cluster beds and studios. The clusters gap has widened in the past couple of months, reaching -2.4 points as of the end of March. The studios gap has also recently widened, reaching a low point of -3.4 points as of the end of February. This did recover slightly last month, finishing at -2.3 points as of the end of March.

Source: StuRents Occupancy Survey

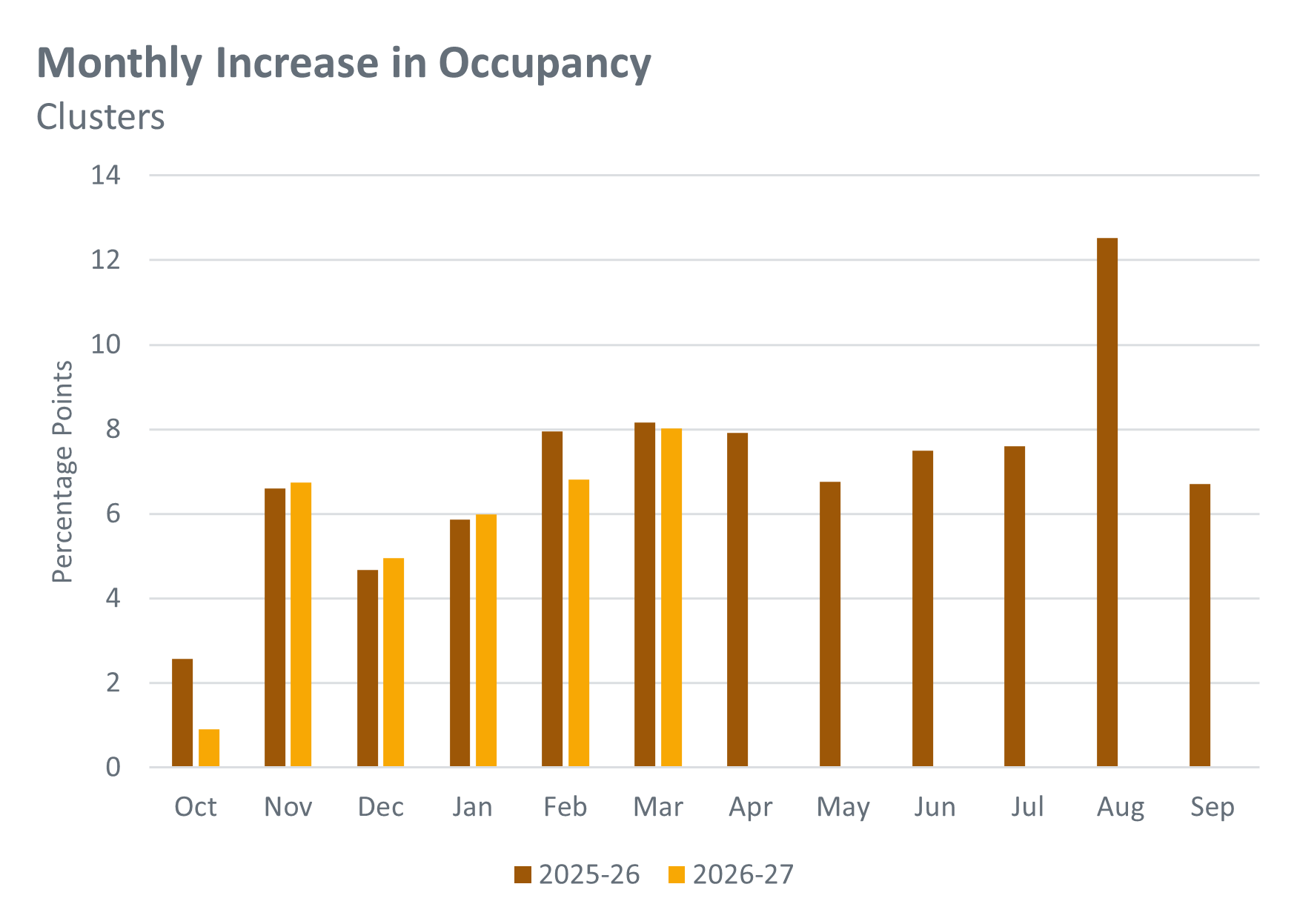

Looking at which months of the cycle have had the biggest gains in cluster occupancy so far, the above chart shows that the pattern is very similar to that of 25-26. A spike in bookings in November was followed by a drop-off, then an increase each month up until March. It remains to be seen whether the pattern will continue to follow, with another decline in bookings per month before the expected surge in the summer.

Source: StuRents Occupancy Survey

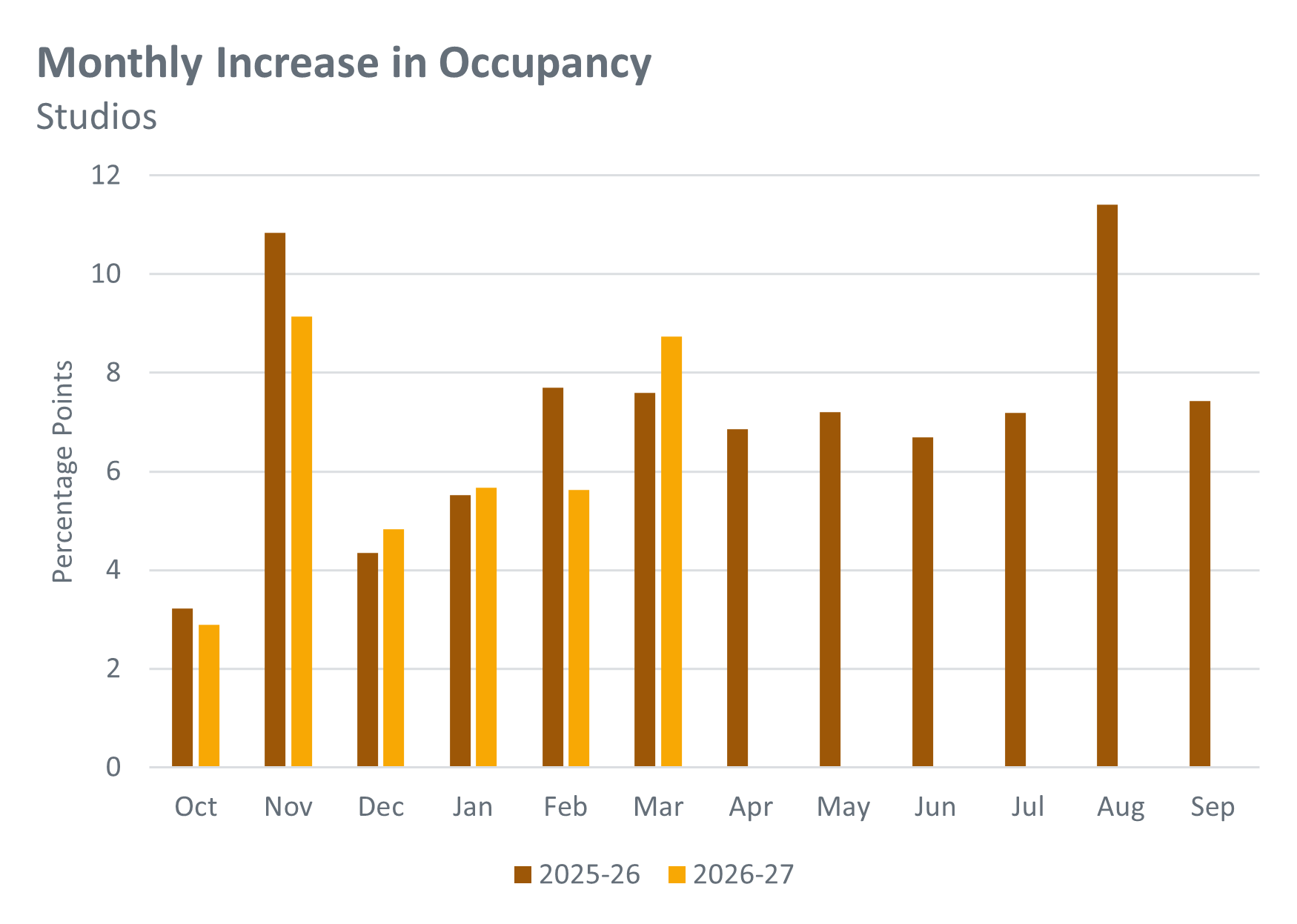

In the same chart but for studios, there is also a match in seasonality compared to 25-26. Again, a spike in bookings in November has been followed by a drop-off, then an increase up to March. The seasonality patterns of this year and last are in contrast to those seen in 24-25, where the market was generally earlier for both clusters and studios.

Source: StuRents Occupancy Survey

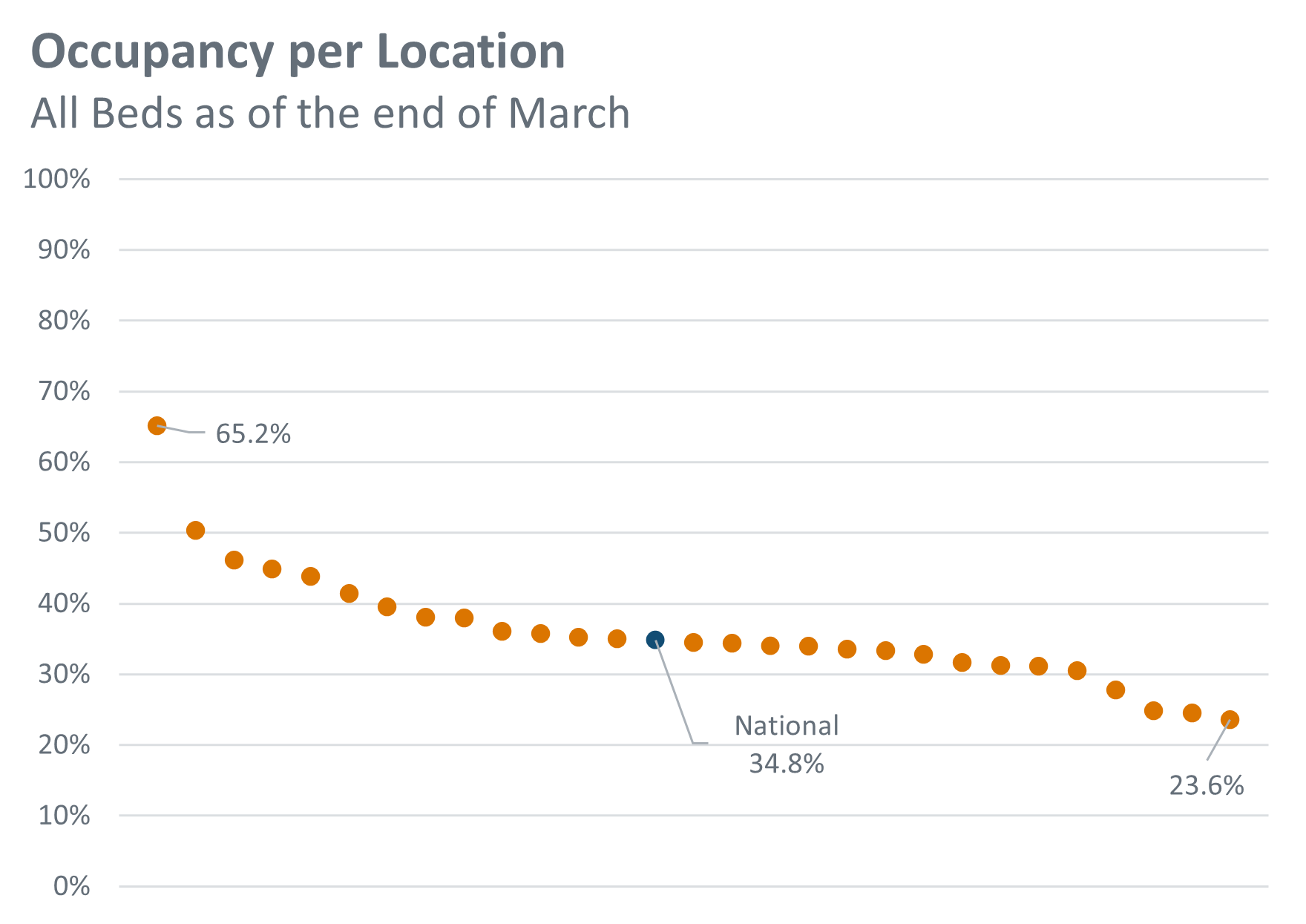

The chart above shows how end-of-March occupancy varies across the 28 locations we cover in the survey, including the national average for comparison. The difference in fortunes is stark, with the highest-performing location recording 65.2% occupancy compared to 23.6% for the lowest. This highlights just how varied the supply and demand dynamics are in different locations across the UK.

Overall, leasing performance for 2026-27 is tracking closely behind last year and continues to lag earlier cycles, with weaker year-on-year occupancy and widening booking gaps in recent months. While seasonal patterns remain consistent, suggesting potential for a summer uplift, the wide variation across locations underlines that local market dynamics will be key to final outcomes.

For more information about our proprietary, highly granular data covering UK student accommodation contact the StuRents Research team today. Book a demo of our Data Portal to find out how you can have up-to-the-minute university housing insights at your fingertips, or get in touch with us about our Occupancy Survey.

Share

Article by

Research Analyst at StuRents

Sam Gillespie is a research analyst in StuRents’ research division, StuRents Intelligence.