StuRents Summit 2026 Recap

We recently hosted the 2026 StuRents Summit at Fulham Pier, bringing together over 200 professionals from operators, owners, investors and marketers. We’ve summarised some of the highlights from presentations and panel discussions, giving insights, expectations and predictions for this year and beyond in the student sector.

Market fundamentals

Source: StuRents, Gov.uk

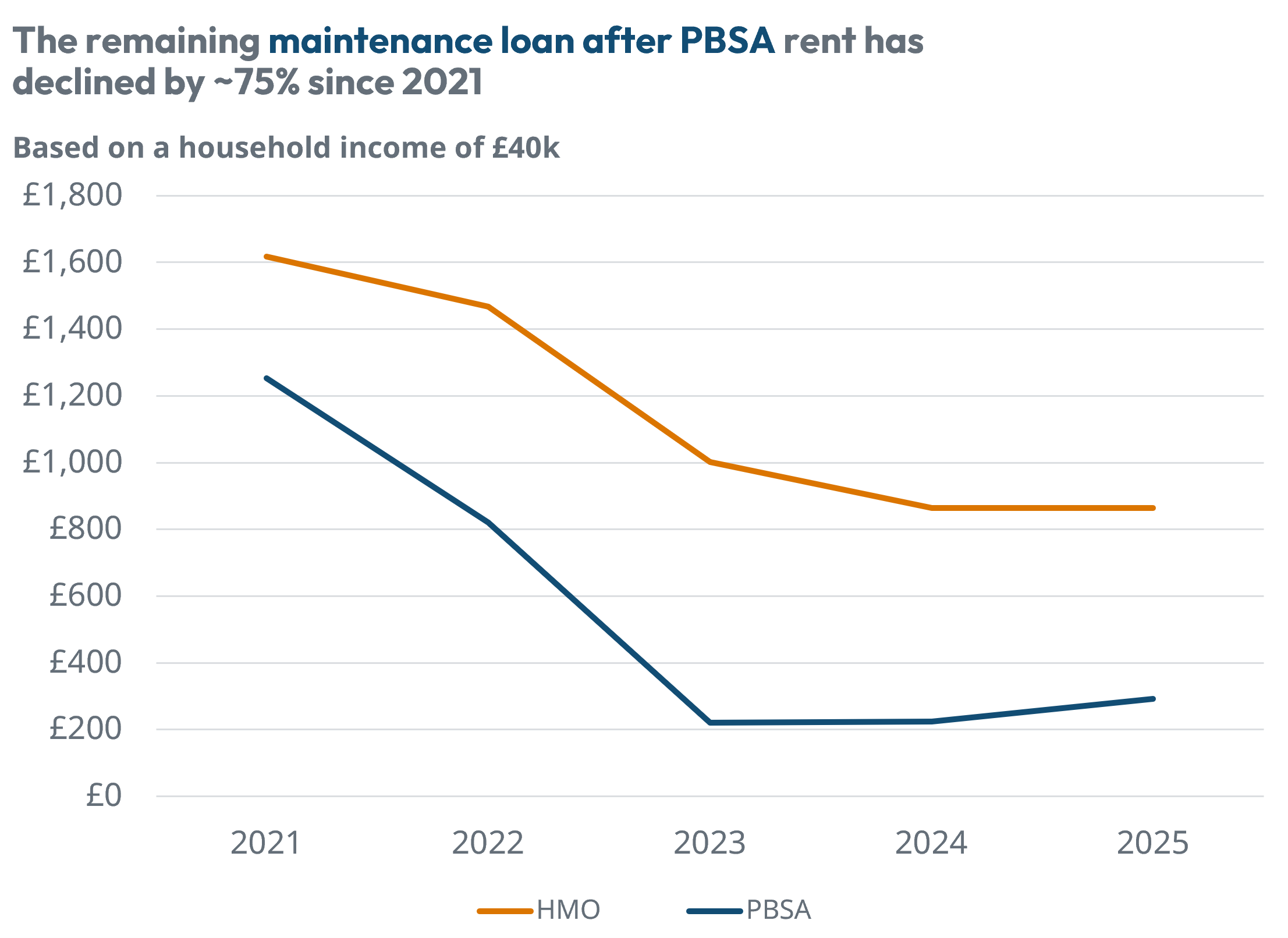

Affordability continues to be a defining trend in the UK student accommodation market. For students from households with an income of £40,000, the amount of maintenance loan remaining after rent has fallen significantly since 2021, with the residual loan roughly halving in both HMOs (from £1,618 to £865) and PBSA (from £1,253 to £293) by 2025. While there has been a modest improvement in PBSA affordability since 2023, students are still left with substantially less funding to cover living costs than they were four years ago. This increasing financial pressure is also influencing international students, who are placing greater emphasis on return on investment when choosing where and what to study.

Source: StuRents, UCAS

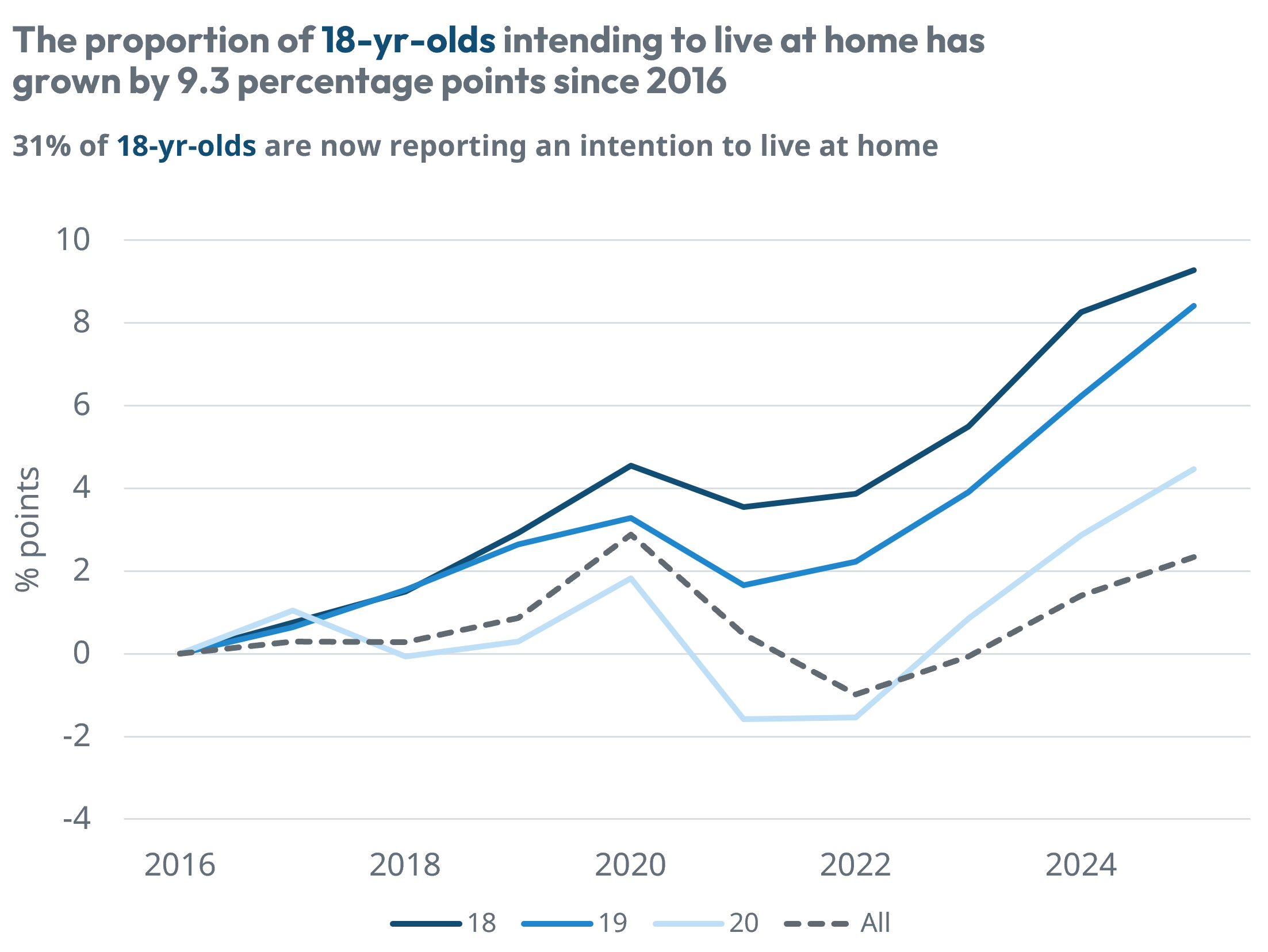

The proportion of prospective undergraduate students intending to live at home has increased steadily across key age groups since 2016, with the strongest growth recorded in 2024 and 2025. Among 18-year-olds, the rate is now 9.3 percentage points above its 2016 level, while the increase has reached 8.4 percentage points for 19-year-olds and 4.5 percentage points for 20-year-olds. The trend reflects growing affordability pressures and a widening gap between student income and living costs, encouraging more students to commute from home. With around two-thirds of students now in paid work alongside their studies, cost considerations are playing an increasingly important role in accommodation choices. As a result, rising commuter student numbers are likely to offset some of the expected growth in demand for student accommodation in the coming years.

Source: StuRents

There is significant variation in booking velocity across the surveyed locations for the 2026–27 academic year. While the national average stands at 43% occupancy at the latest reporting point, performance can range from just 30% in the slower-moving market to 67% in the stronger ones. Several locations are tracking well ahead of the national benchmark, while others remain materially behind, underlining the highly localised nature of student accommodation markets.

Competing supply pools

Source: StuRents

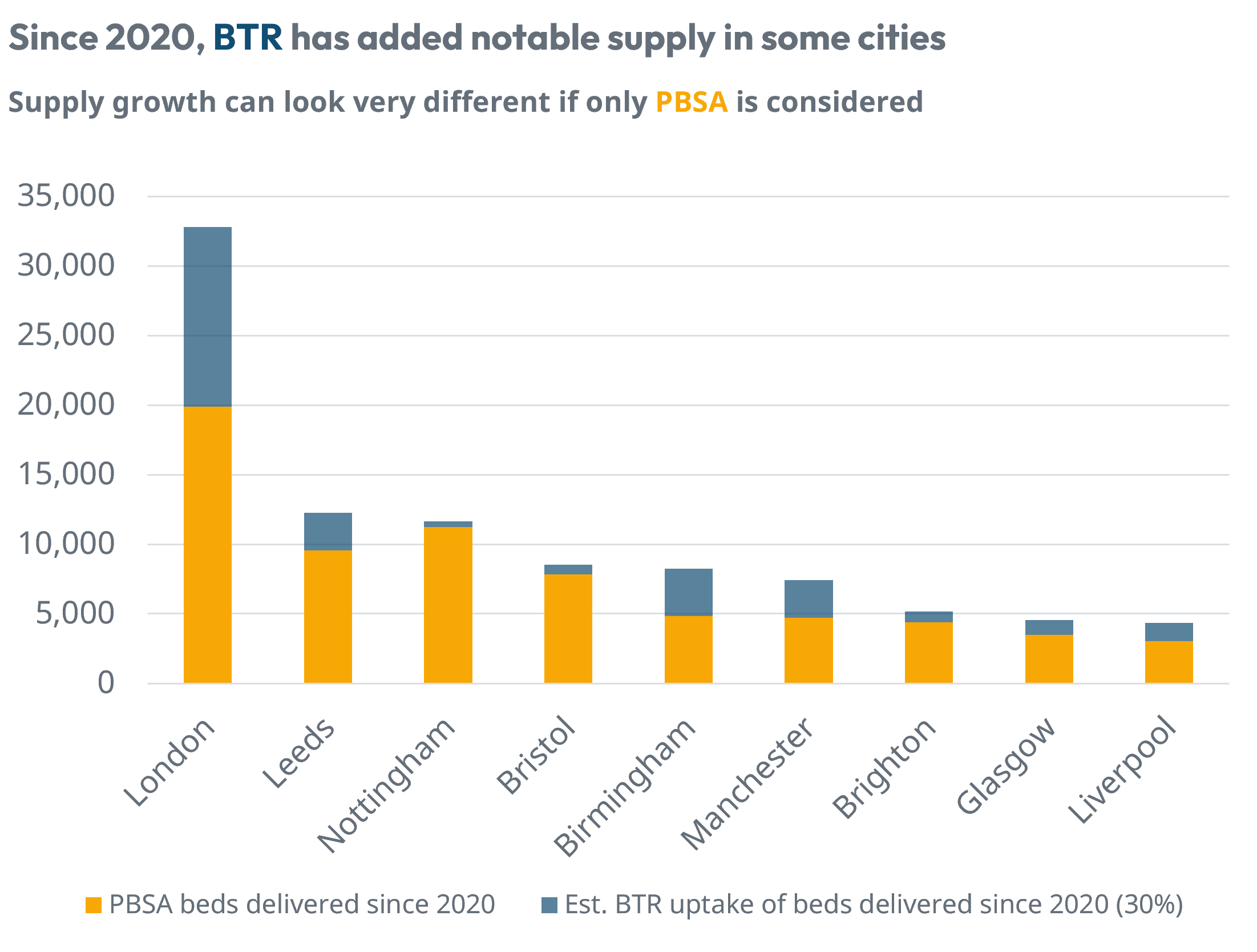

The growth of Build-to-Rent (BTR) development is increasingly influencing student accommodation markets and, in some cities, materially altering the supply and demand outlook. Assuming 30% of BTR residents are students, the sector has effectively added the equivalent of almost 13,000 student beds in London since 2020, alongside meaningful contributions in cities such as Birmingham, Manchester, Liverpool and Leeds. This additional capacity is often overlooked when assessing market balance, creating a risk of capital being misallocated towards new PBSA developments in locations where alternative forms of accommodation are already absorbing student demand. The emergence of co-living and other professionally managed rental products is likely to reinforce this trend, further blurring the distinction between traditional student and residential housing markets.

Opportunities and outlook

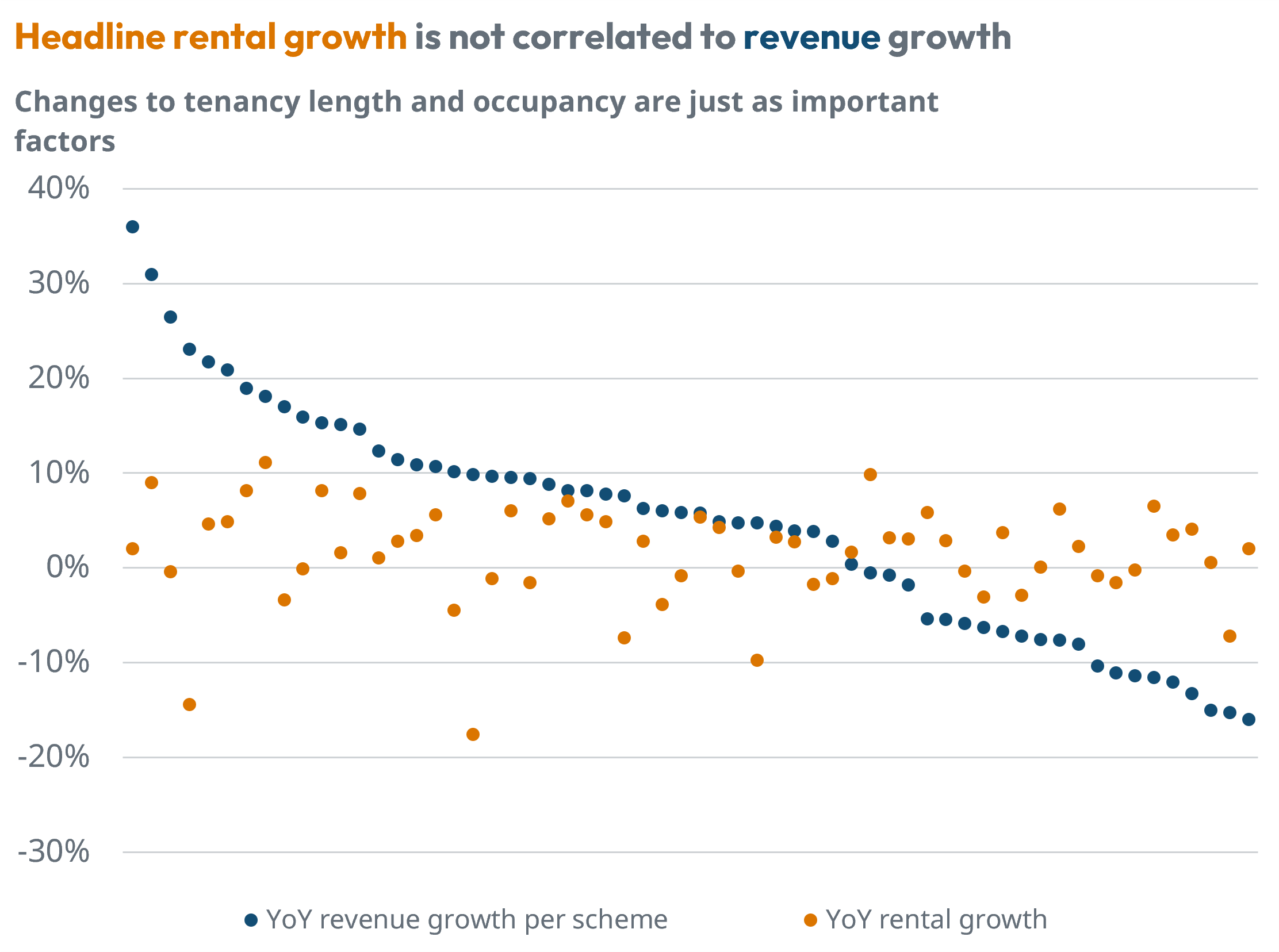

Source: StuRents

This data highlights a clear disconnect between headline rental growth and revenue performance at the scheme level. While some assets achieved revenue growth of more than 20% despite only modest rental increases, others recorded declining revenues even as rents continued to rise. This demonstrates that revenue growth is influenced by a range of factors beyond rental rates alone, including operational costs, occupancy levels, and discounting and incentive strategies. For operators and investors, this presents both opportunity and risk: strong operational performance can drive significant revenue gains without relying on aggressive rent growth, while an overemphasis on rental increases may mask underlying occupancy challenges and lead to weaker overall financial outcomes.

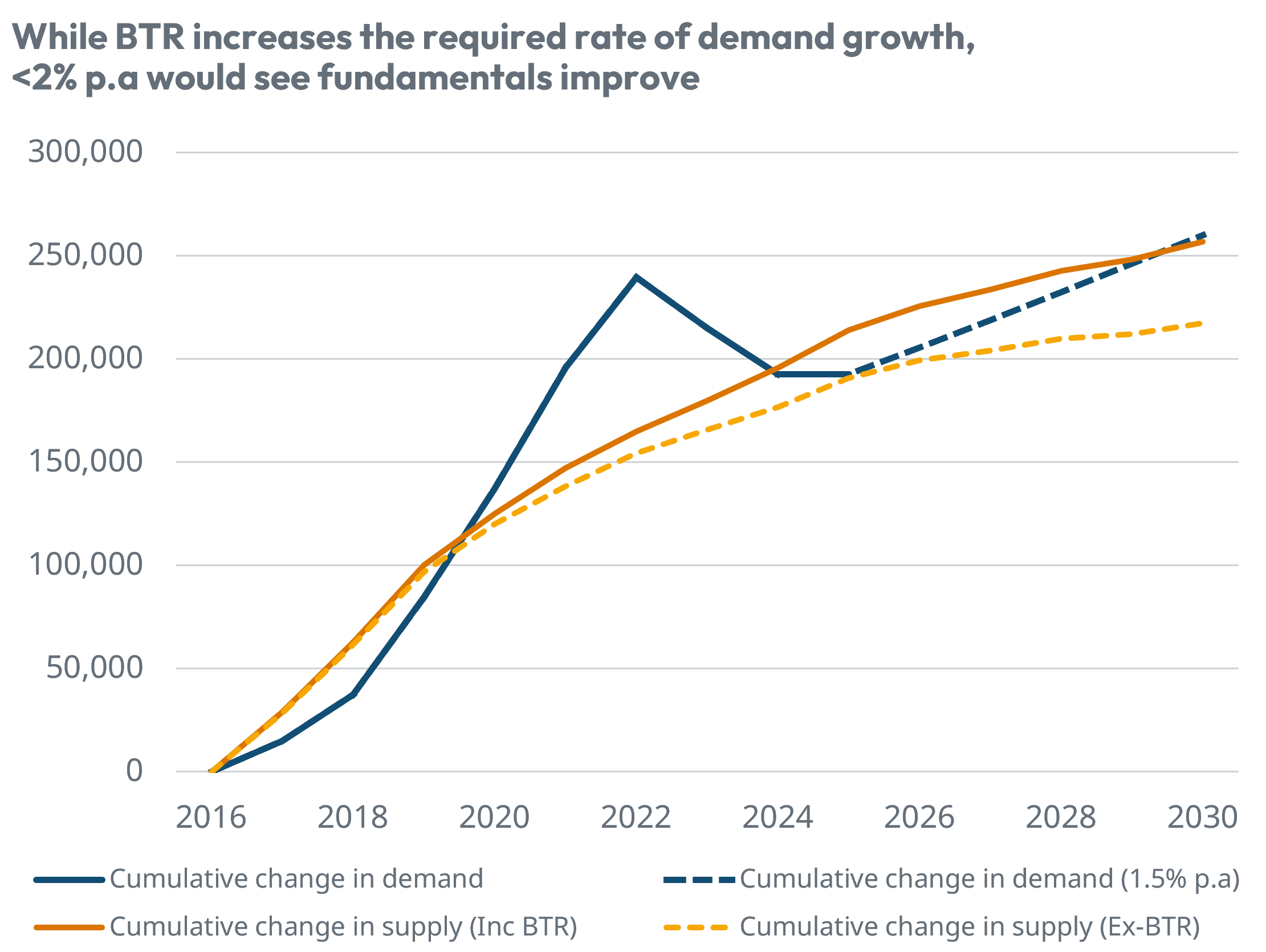

Source: StuRents

The data shows a long-term tightening in the supply vs demand balance across UK PBSA markets (excluding London), with cumulative demand broadly outpacing supply under most scenarios. However, the outlook is complicated by structural factors, including scheme withdrawals, a rising “live at home” cohort, and potential university consolidation or mergers, all of which dampen effective demand growth. While the inclusion of BTR meaningfully increases the required rate of demand growth to maintain balance, the projections suggest that even at sub-2% annual demand growth, underlying fundamentals continue to improve over time. This points to a market that is more nuanced than headline demand figures suggest, with localised pressures likely to remain.

An impartial review: Student Demand in 2026 and beyond

Our first panel of the day, hosted by our Head of Research Richard Ward, saw Paul Watson (MD of Now Students), Matt Walker (CEO of Mapletree), Tom Ferber (Founder of Homie) and Sam Rason (Co-founder of VIVA) explore how student demand is normalising after the post-Covid boom, with performance now varying heavily by market, university, and student profile.

Student demand is changing, but the story is more nuanced than "up” or “down”.

A few themes stood out:

- Students are behaving more like value-conscious consumers, with less incentive to book early if later deals or better terms are available.

- International demand is shifting, with some markets seeing a decline in Chinese students, while India continues to grow in importance.

- Chinese students are also becoming more selective, looking closely at university reputation, career prospects, lifestyle, and what other students are saying online.

Battle of the beds: A comparison of asset classes and investment strategies

The second panel, hosted by Jessica Middleton-Pugh of Green Street News, saw Ioannis Verdelis (MD of Landmark Properties), Raoul Malhotra (CEO of Orka), Victoria Campbell (CEO of TriBell), and Lucy Keeling (Associate Director at Colliers) discuss how different living sectors compete, overlap, and, in some cases, complement one another.

The “battle of the beds” isn’t simply PBSA vs BTR vs co-living vs HMOs.

Some key takeaways:

- Micro-location matters more than ever. The strength of the university, distance from campus, local amenities and even which side of the road an asset sits on can all shape demand and pricing.

- Affordability is also changing the conversation. Not every scheme needs to be the most premium product in the market. For many operators, the opportunity is in creating a compelling, well-located offer that matches what students can realistically afford.

- HMOs remain a highly stable part of the market, while PBSA, BTR and co-living continue to compete differently depending on the city, student profile and available supply.

- There is still opportunity across living sectors, but success depends on understanding the local market, pricing carefully, and knowing exactly who the product is for.

A sector pulse check: Understanding the university outlook, operational cost challenges, and sector returns

Our third and final panel of the day, hosted by Paddy Jackman (consultant at JESL), saw Niamh O’Connor (Partner at SUMMIX), Saurabh Arora (Co-founder & CEO of University Living), Brian Welsh (Founder and CEO of OPRE), and Karen Best (Partner at PWC) take the pulse of the sector, covering university finances, international demand, development viability, investor appetite and the future of PBSA.

The student accommodation sector is still full of opportunity, but the routes to finding it are becoming more complex.

Some interesting points were raised:

- Universities may need to move beyond tactical fixes and make more structural decisions around size, specialisation and collaboration.

- Investors are also looking harder at market resilience, with more research going into secondary cities, international demand patterns and alternative end-user scenarios.

- For PBSA, viability remains a challenge. Construction costs, regulation and longer hold periods mean schemes need to be underwritten with more flexibility than before.

But the message wasn’t negative. Well-located student accommodation still has a clear role to play, especially where operators and investors understand the local market, the university context and the changing shape of international demand.

Register your interest for our 2027 Summit here.

For more information about our proprietary, highly granular data covering UK student accommodation contact the StuRents Research team today. Book a demo of our Data Portal to find out how you can have up-to-the-minute university housing insights at your fingertips, or get in touch with us about our Occupancy Survey.

Share

Article by

Research Analyst at StuRents

Sam Gillespie is a research analyst in StuRents’ research division, StuRents Intelligence.