Occupancy Update – May 2026

Image courtesy of Flickr

We’re now eight months into the 2026-27 PBSA leasing cycle, and this update explores how the market has progressed through the end of May, analysing booking trends, year-on-year performance, and seasonal patterns by bed type. The survey continues to provide the most comprehensive view of UK PBSA leasing activity available, capturing around 50% of the private PBSA direct-let market and offering valuable insight into current dynamics across all major student accommodation markets.

StuRents Occupancy Survey includes private PBSA direct-let bookings only. University halls and private beds on nomination agreements are excluded.

Source: StuRents Occupancy Survey

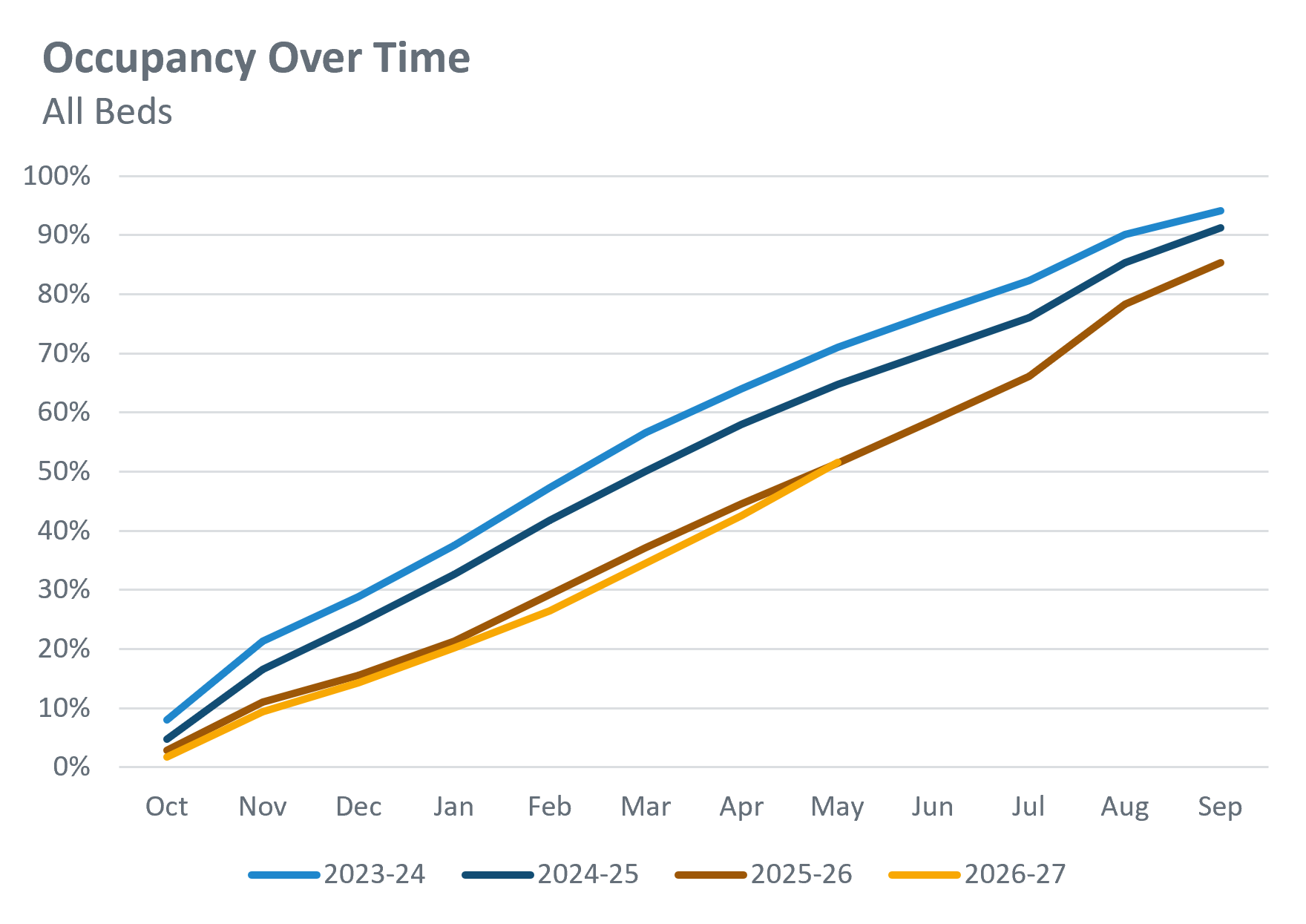

The above chart is showing how 26-27 leasing velocity has ‘caught up’ with that of 25-26 after slightly lagging behind for most of the cycle. Across all bed types in all 28 locations we cover, average occupancy for 26-27 stood at 51.6% as of the end of May. This represents a 0.1 percentage point increase year-on-year (YoY).

Source: StuRents Occupancy Survey

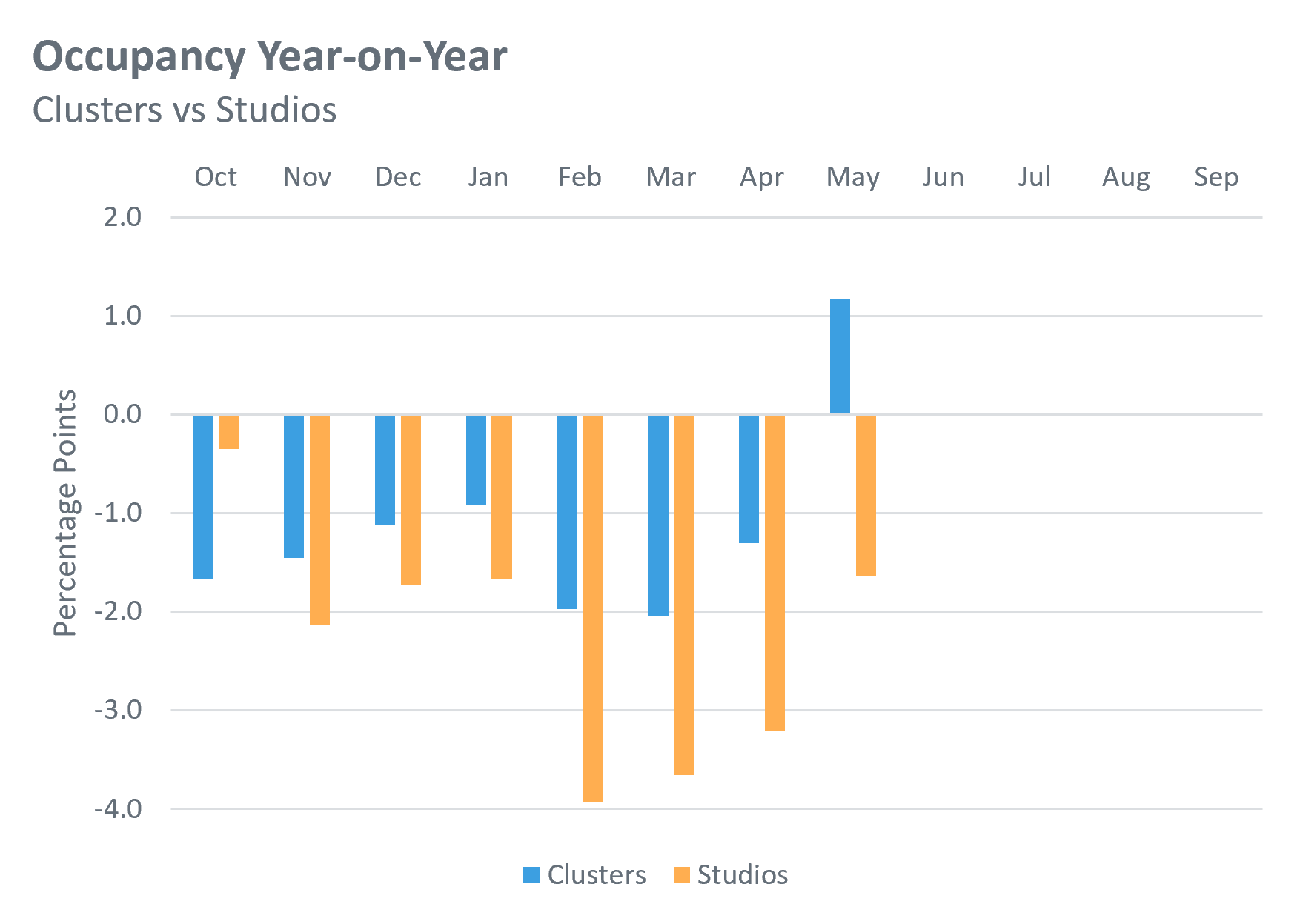

This chart is showing how the YoY gap in bookings has changed throughout the cycle so far for both cluster beds and studios. The clusters gap switched from negative to positive in May – from -1.3 percentage points down to 1.2 points up. The studios gap has narrowed for the third consecutive month and is now 1.6 points down on last year.

Source: StuRents Occupancy Survey

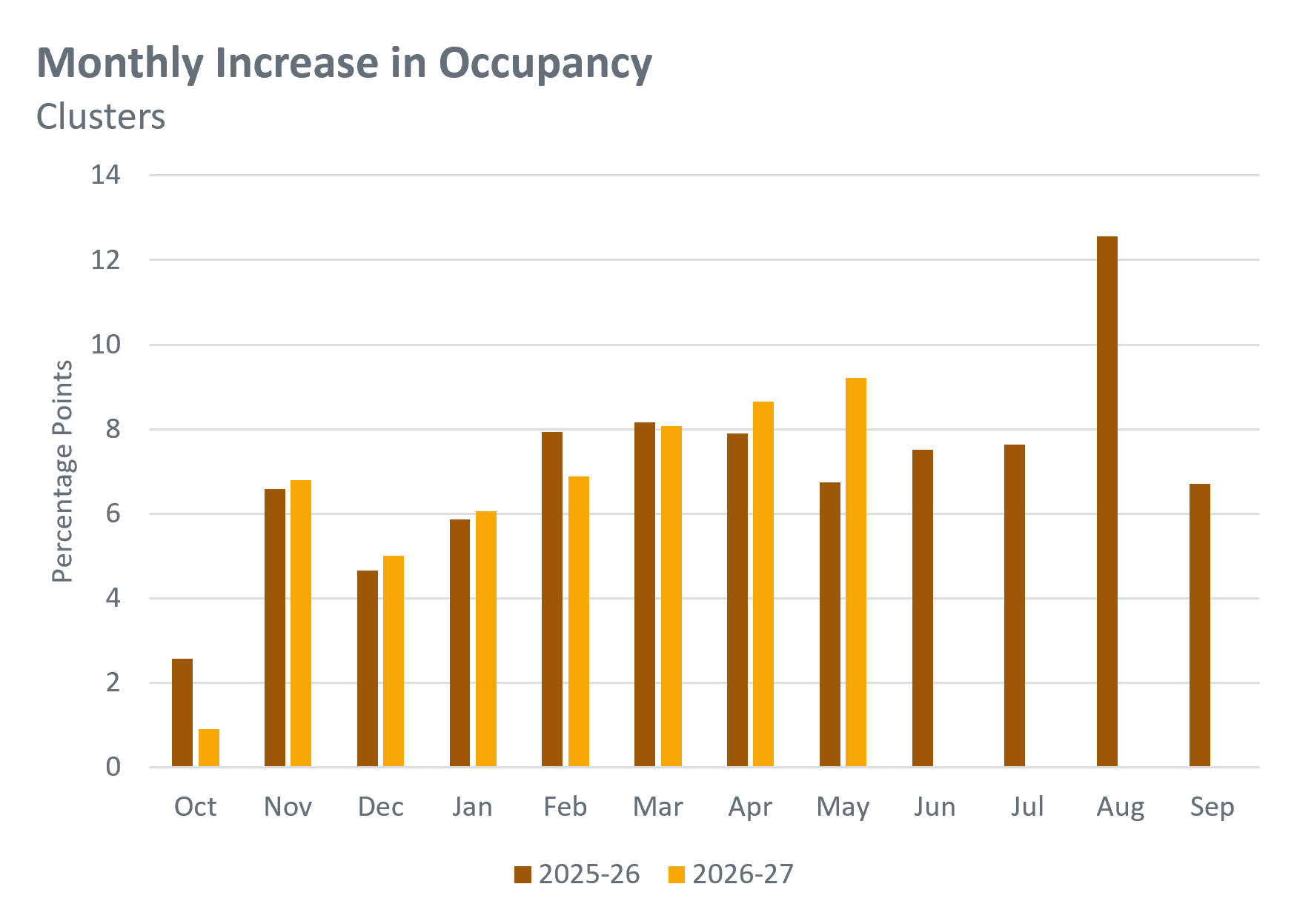

Looking at which months of the cycle have had the biggest gains in cluster occupancy so far, the above chart shows that May was the best month for bookings yet, with an increase of 9.2 points recorded. This goes somewhat against the pattern observed last year, where there was a drop-off in bookings in the early spring/summer months.

Source: StuRents Occupancy Survey

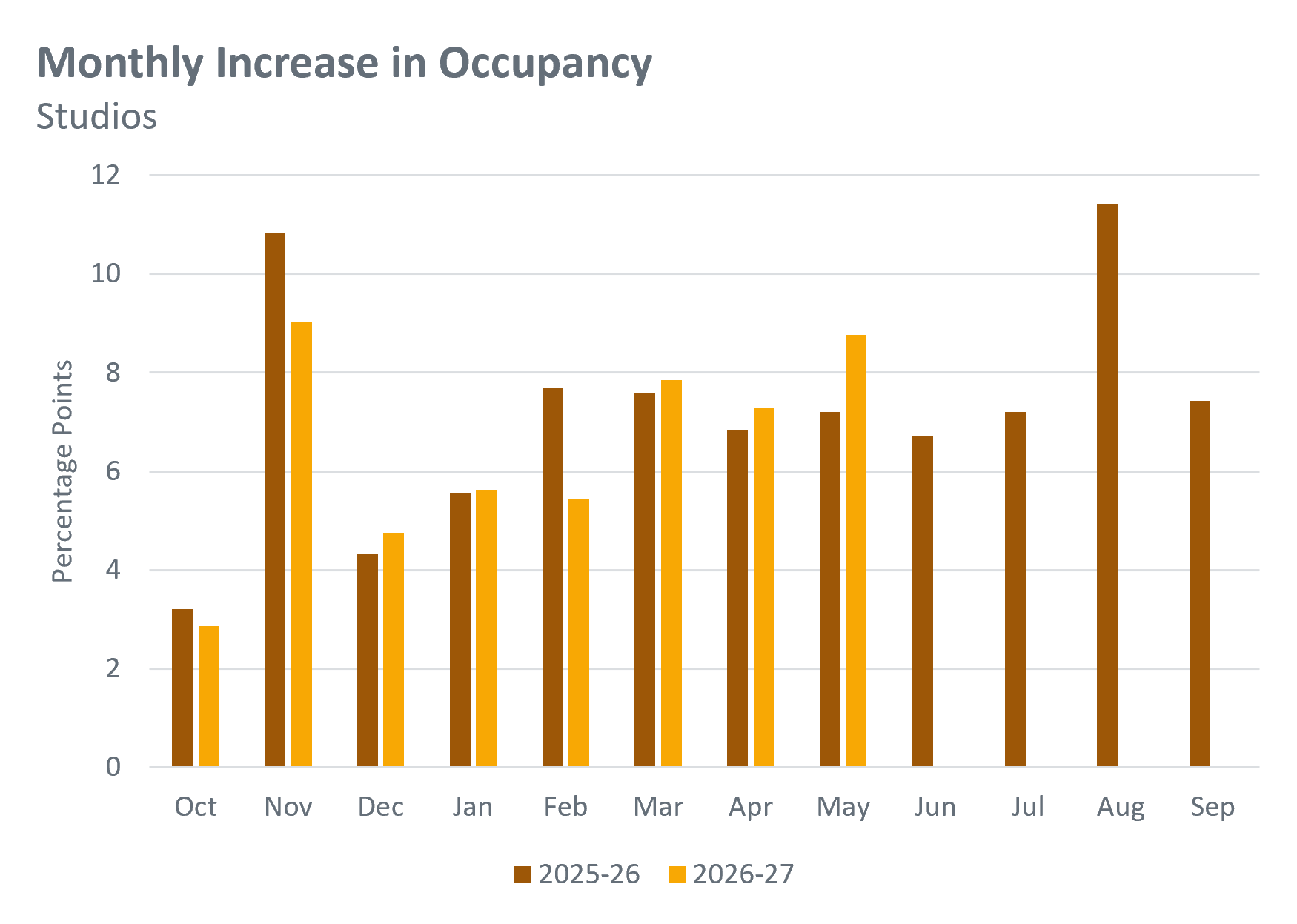

For studios, May recorded a stronger month-on-month increase than the equivalent period last year (8.8 percentage points versus 7.2) and was the strongest month since November. Again, this contrasts last year’s pattern, where a drop-off was recorded in this period.

Source: StuRents Occupancy Survey

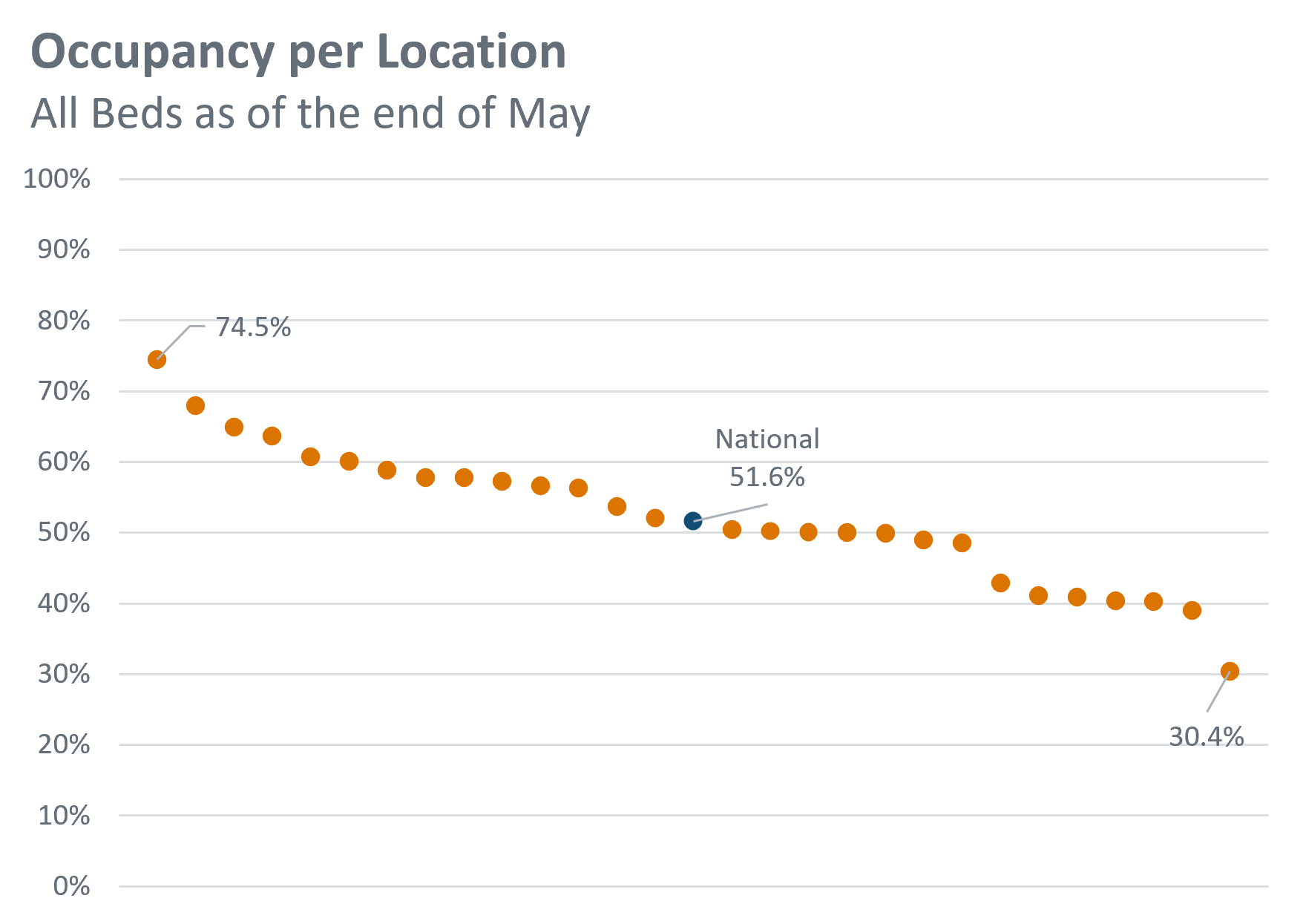

The chart above compares end-of-May occupancy across the 28 survey locations, alongside the national average. Performance continues to vary considerably, with occupancy levels ranging from 74.5% in the highest-performing location to 30.4% in the lowest. These wide disparities reflect the differing supply and demand conditions that exist across local accommodation markets in the UK.

Overall, leasing performance for 2026-27 is tracking closely to last year and continues to lag earlier cycles. However, as always, the devil is in the detail, as dynamics can vary significantly when the data is broken down by bed type and/or location.

For more information about our proprietary, highly granular data covering UK student accommodation, contact the StuRents Research team today. Book a demo of our Data Portal to find out how you can have up-to-the-minute university housing insights at your fingertips, or get in touch with us about our Occupancy Survey.

Share

Article by

Research Analyst at StuRents

Sam Gillespie is a research analyst in StuRents’ research division, StuRents Intelligence.