Student Accommodation Research: Q2-2021 Market Update

Demand Growth

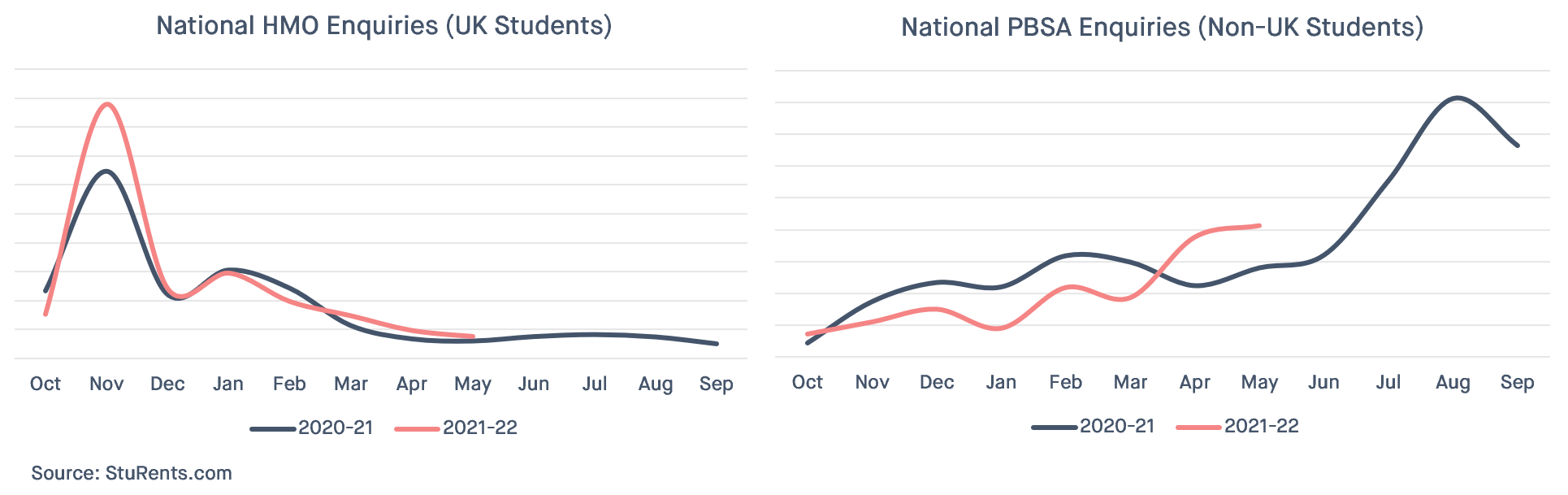

At the height of the pandemic last year, many in the sector would have hoped that the 2021-22 season would represent a return to the status quo. However, our latest data suggests this has not been the case, with a divergence in performance between accommodation types.

Whilst enquiries for PBSA are picking up and have begun to overtake levels recorded during the equivalent period of last year, the timing coincides with a fall in activity that occurred as the UK entered its first lockdown in Mar-20, thereby skewing year-on-year comparisons. Nevertheless, PBSA demand is down year-to-date, suggesting a protracted lettings cycle for 2021-22.

More positively with lockdown measures easing and the successful rollout of the vaccine, demand should continue to climb through the summer. However, announcements by universities that teaching could remain online into the autumn may dampen demand, along with the rise of new variants such as the Indian variety which could restrict international travel.

In contrast to PBSA, demand for HMOs has marched on unabated and was extremely strong at the start of the season. Enquiries are up year-on-year and with the 18-year-old population on the rise, the prime target market for HMOs, this accommodation type could be a big beneficiary in the coming years.

Figure 1: National Year-on-Year Enquiry Growth

NB: The 2021-22 lettings cycle refers to the period Oct-2020 to Sep-2021

Planning

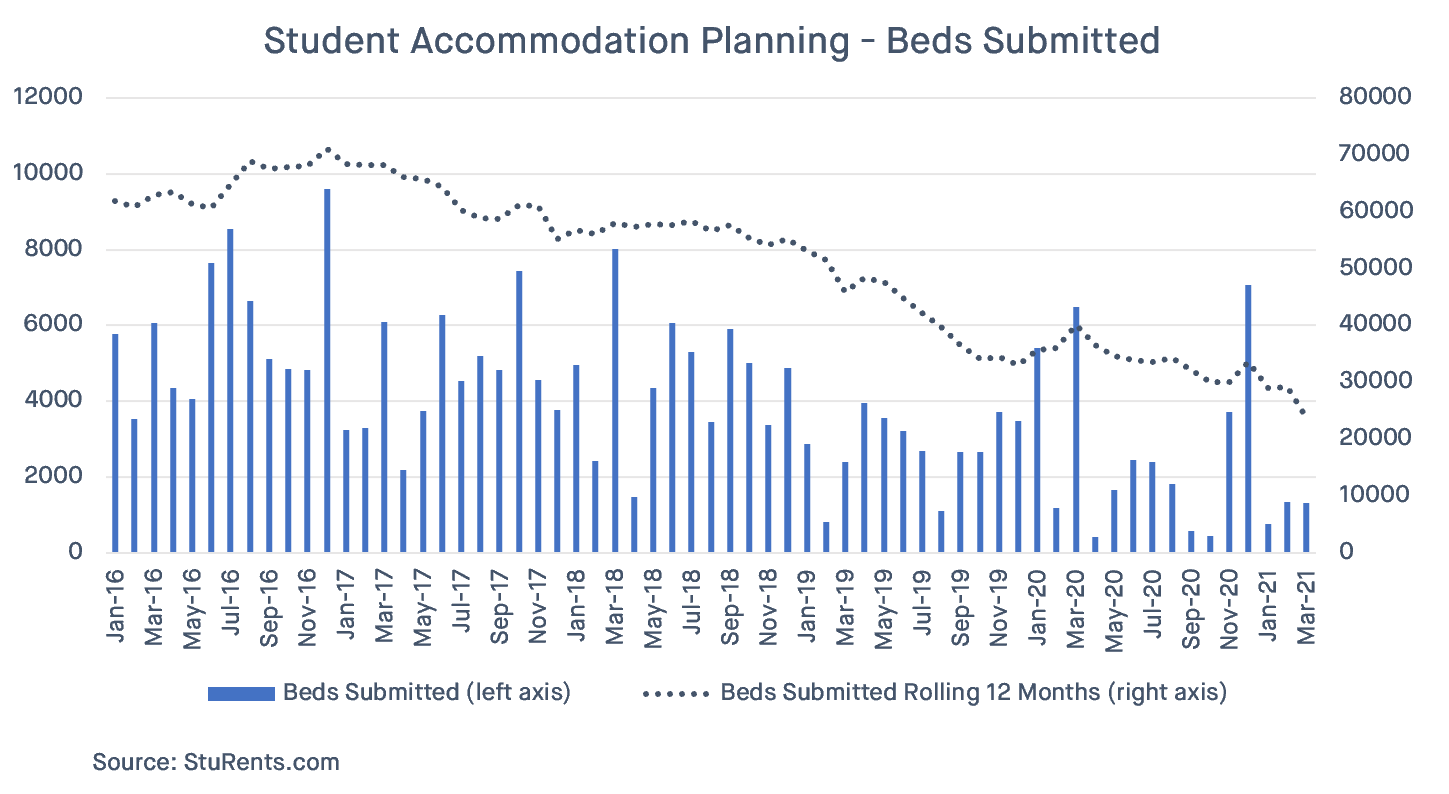

Planning application activity was subdued in the first three months of 2021, with net planning applications totalling fewer than 3,500 beds put forward. This represents a noticeable slowdown compared to the 11k units lodged in the final quarter of 2020. Figure 2 highlights that this trend is consistent with the general slowdown in planning activity that has been recorded since 2016.

Despite the limited number of new schemes put forward in the last quarter, some of the most notable planning updates include:

- The approval of a huge 950-bed scheme in Birmingham close to Adderly Street

- The refusal of Hines' 1,000+ bed development in Birmingham

- The submission of a 534-bed scheme on behalf of Fusion Students in Manchester

- The submission of 557 beds on behalf of iQ Student in Glasgow

- Nine new applications in Nottingham totalling >1,000 beds with a large proportion being all-studio schemes

- The approval of an all-studio scheme from Bricks Capital (True Student) for 475 beds in Leicester

- The approval of a 328-bed development in Swansea

Figure 2: Planning Application Activity - Beds Submitted

Student vs Supply Growth

One of the driving forces behind the slowdown in planning is changing market fundamentals across some of the larger university cities, which have historically been a hotbed of activity.

It is well reported that markets such as Sheffield face challenging fundamentals for operators of PBSA, albeit as always, the success of a scheme will depend on intra-city dynamics. As a result, planning activity has contracted sharply.

When considering the historic growth in new PBSA supply vs new demand it is easy to see why.

Cumulative PBSA growth has far outstripped demand growth by a substantial margin as indicated in Figure 3. Therefore, unless a noticeable proportion of existing supply is removed from the market, PBSA will need to draw students out of HMOs to make up for this shortfall. However, for the average budget-conscious domestic student, the price differential between HMOs and PBSA may simply be too large to bridge. This is particularly true if rent consumes most or all of a students maintenance loan.

In markets such as Newcastle, operators have had to adjust their pricing accordingly. PBSA rooms can now be booked for less than £100pppw, ensuring they compete directly with HMOs on price.

Figure 3: Cumulative Change in Demand vs Supply for purpose built student accommodation in Sheffield

The question for investors to then consider is which locations do fundamentals remain attractive going forward and which will face significant headwinds due to an imbalance between supply and demand growth.

Arguably, measures such as the Student to Bed Ratio are no longer adequate as they offer a one-dimensional snapshot of the sector, ignore the role HMOs play and overestimate the addressable market for PBSA.

Institutional capital is increasingly aware of this and other nuances of the market. Some are even considering the HMO sector. With the 18-year-old population set to rise substantially in the years ahead and restrictions on the delivery of new supply via measures such as Article 4, arguably the fundamentals for HMOs are just as, if not more attractive. However, HMOs do come with their own challenges, not to mention the difficulty in deploying capital at scale, relative to PBSA.

To understand more about our market leading analytics Register Here.

About StuRents:

- StuRents is one of the leading proptech partners in the UK student accommodation space

- StuRents operates StuRents.com, the largest student-centric accommodation search platform, listing over 750,000 bed spaces nationwide

- Beyond search, StuRents facilitates integrated online tenancy signing, tenancy payments and app-based tenancy management solutions

- This unique, vertically integrated end-to-end solution underpins StuRents' data insights and research capabilities

Share

Article by

Head of Research at StuRents

Richard leads the StuRents research team, providing proprietary, platform-driven insights to help stakeholders make better-informed decisions about the market.