Student Accommodation Research: Q2-2020 Market Update

Planning activity

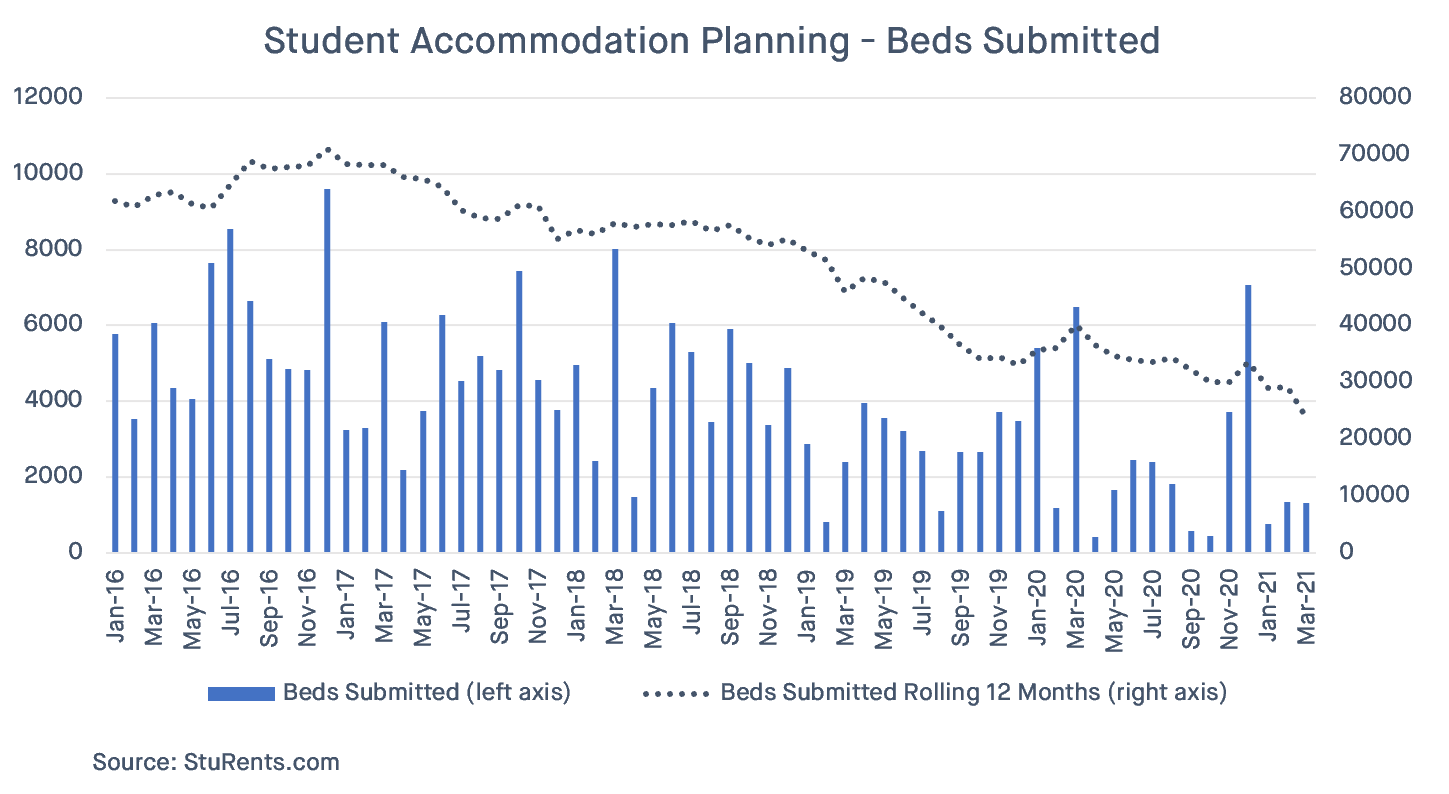

In the last quarter (Jan-Mar), planning activity remained robust, with applications totalling more than 12,000 beds put forward, compared to fewer than 8,000 lodged in the same period of 2019. However, just over 4,000 beds have been granted planning permission year-to-date, versus more than 5,000 in the first three months of 2019.

Although more applications were submitted in the first quarter of 2020 compared to last year, the long-term trend suggests a slowdown in activity. Figure 1 highlights that since peaking in 2016, the number of beds submitted and approved each year has been in decline.

Figure 1: Number of beds submitted and approved

Source: StuRents.com

However, the national trend hides significant differences between individual cities. One of the most active locations for planning activity in the last quarter was Edinburgh, with seven new developments put forward. Combined, these applications contained just under 1,500 beds, which surpassed the number of units lodged through the whole of 2018.

Elsewhere, Unite Students was granted planning permission for a huge new scheme in Nottingham, which helped take the total number of beds approved to more than 1,200 in the first quarter of 2020 alone. Nottingham is just one example of a city that has seen a significant amount of planning application activity in the past two years, contradicting the national trend.

Similarly, in Birmingham more beds were put forward in the first three months of 2020 than in the whole of 2019. The largest scheme, submitted by Hines and to be managed by Aparto Student, contains more than 1,100 beds.

Market Seasonality

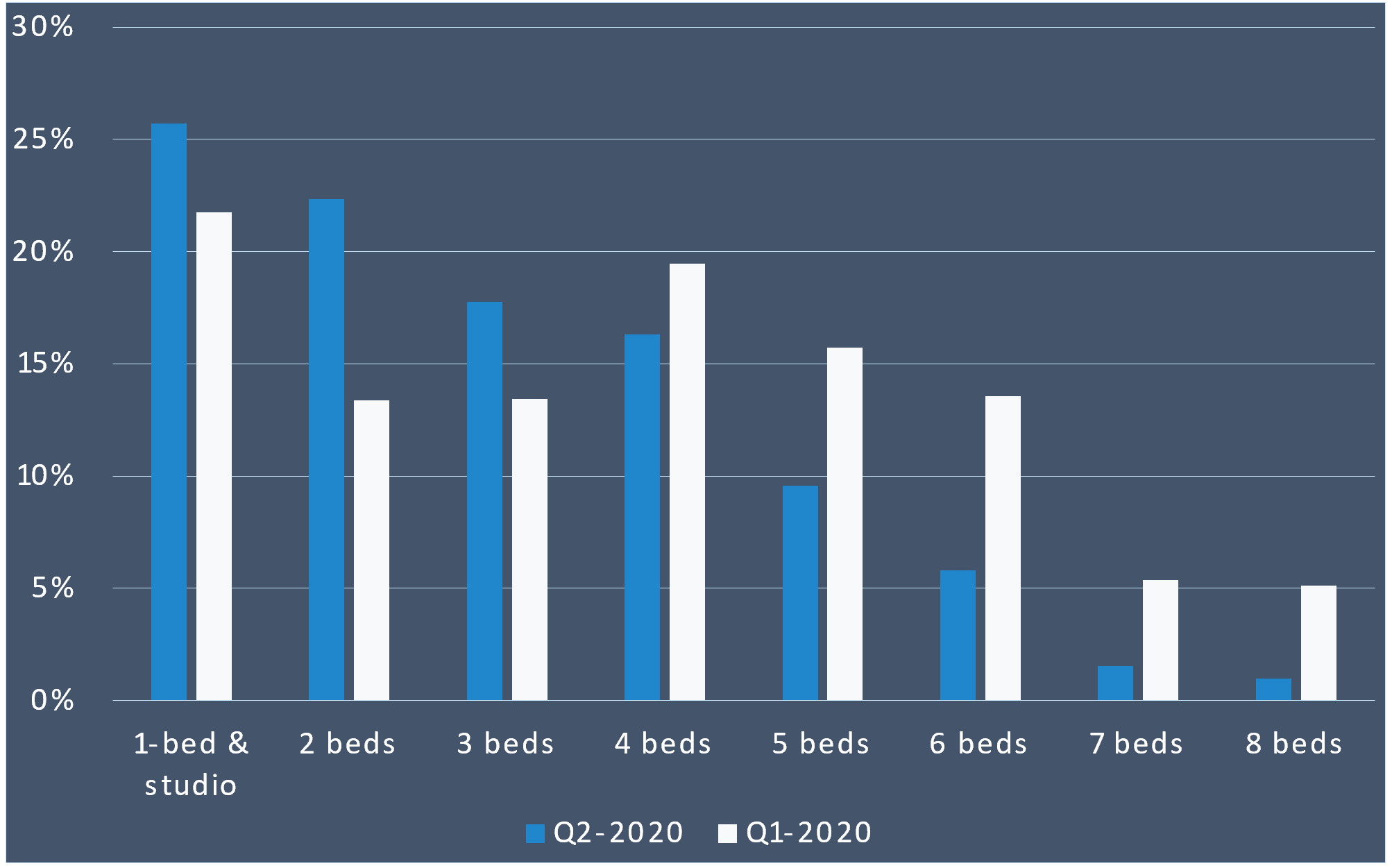

On a national basis, in the last quarter (Jan-Mar) smaller sizes grew in popularity, at the expense of larger clusters and houses in multiple occupation (HMOs).

As highlighted in Figure 2, 1-bed flats and studios captured more than 25.0% of all searches on the platform, making it the preferred choice in the last three months. The second most popular choice was 4 beds, which achieved a search share of 16.3%, down from 19.5% in the previous quarter.

Combined, clusters and HMOs containing at least 3 beds, equated to 52.0% of searches performed on the platform. Whilst this still represents a significant proportion of demand, it is noticeably lower than the figure of 72.7% reported in Q1-2020 (Oct-Dec).

The popularity of 2 beds also increased in Q2-2020 (Jan-Mar), with 22.3% of demand attributed to this size, compared to 13.4% reported in the previous quarter.

Looking ahead, we would expect demand to become more skewed towards smaller sizes in the next quarter, with clusters and HMOs capturing a reduced share of demand. With the current social distancing measures in place, some market commentators may expect studios and 1-bed flats to be more popular than they have been historically. However, StuRents' data year-to-date does not suggest this to be the case, with the increasing popularity of these sizes attributed to seasonality fluctuations rather than a fundamental shift in demand.

Figure 2: Proportion of searches by bed size

Source: StuRents.com

Covid-19

Covid-19 has created a significant amount of uncertainty for the market, with questions outstanding on when the new academic year is likely to start, how social distancing will impact teaching and whether institutions will have the financial clout to survive the pandemic.

A recent survey conducted by UCAS and YouthSight suggested 86% of applicants studying A levels said they were continuing with their applications as planned. However, value for money has become a determining factor for students. Growth in full-time students at Russell Group universities highlights this point well, with numbers at these institutions growing by 21.8% between 2012-2018, compared to 12.0% nationally.

One could easily question the perceived value for money in spending £9,250 a year on tuition fees for 'virtual' learning, which could end up curtailing demand for 2020-21 or further exacerbating this flight to quality.

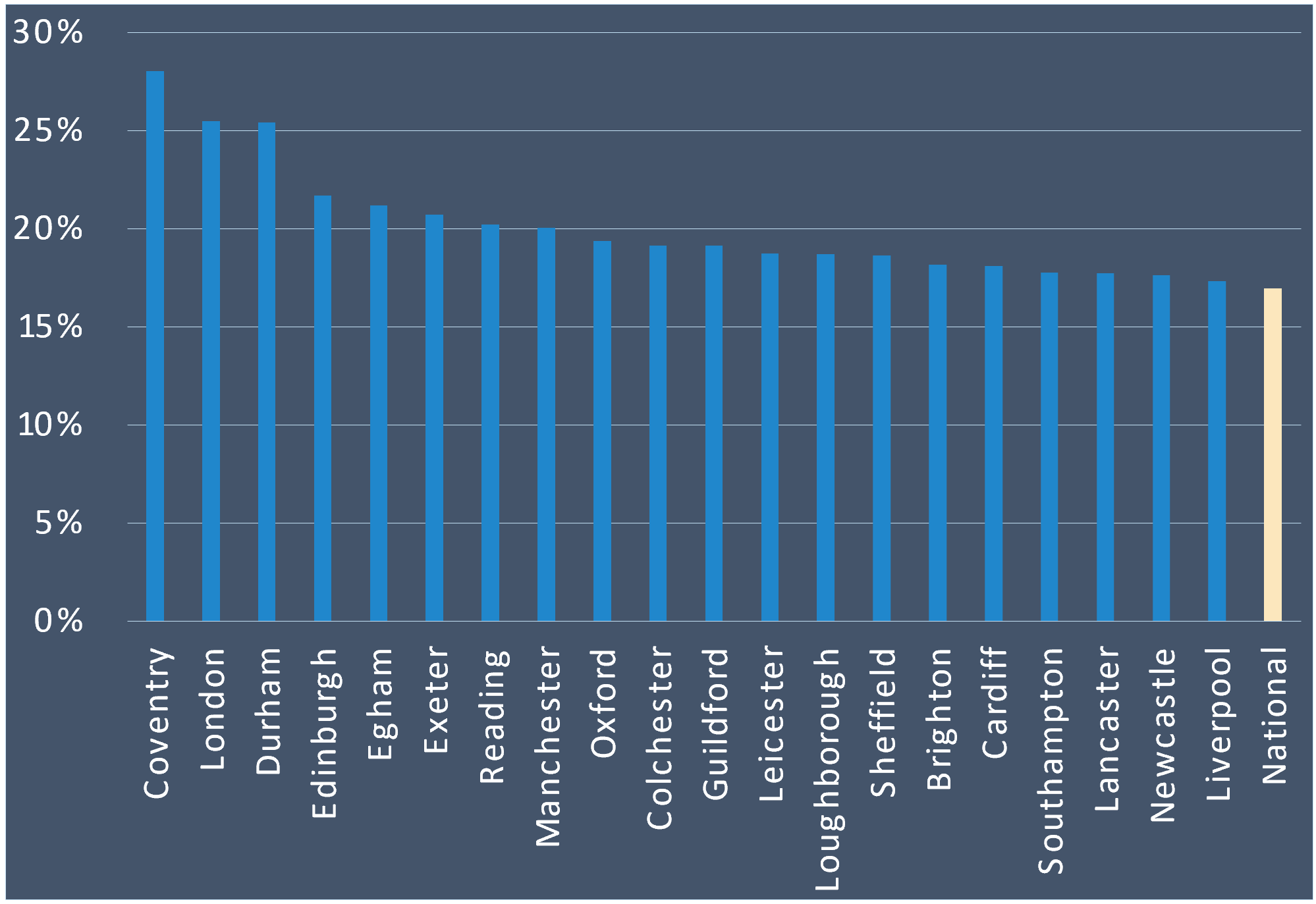

Some of the more prestigious universities have also increasingly relied on income from international students. For these institutions more than others, coronavirus could create a shortfall in students that needs plugging, leaving less attractive universities at risk of losing out. For operators of purpose-built student accommodation (PBSA) in locations over-reliant on overseas students, marketing managers may face the prospect of competing over a smaller demand pool.

One of the most highly exposed locations is Coventry, which has witnessed extraordinary growth in recent years. In 2018 28.0% of full-time students were domiciled from outside the EU, whilst more than 3,200 PBSA beds were added to the market in 2019, with thousands more in the pipeline. If the PBSA sector for international students does become a buyers' market, higher-priced operators without a unique selling point (USP) may struggle to justify their premium compared to the competition.

To counter this risk, some PBSA operators have already expressed their intent to capture a proportion of the market that would typically live in HMOs. However, this may be easier said than done. StuRents' data highlights that outside of London, PBSA on average carries an advertised per person per week premium of c.32.0%, suggesting substantial discounting may be needed to persuade this type of customer to make the switch from HMO to PBSA. For the highest priced accommodation, the discounts required to attract domestic students are likely to be too large to overcome.

Despite the short-term uncertainty, the long-term fundamentals for the sector remain positive. An income-producing, recession resilient asset class should remain attractive for investors, even if stakeholders must select their opportunities more wisely. Furthermore, with the number of 18-year-olds in the country also set to expand in the coming years, the total demand pool should remain favourable. Whether new supply entering the market will meet the requirements of this demand will depend on the affordability of the development, as well as local dynamics, whilst the rapid rise in both quantity and quality of universities in Asia and in particular China could also become a factor in a post-Covid-19 higher education market.

Figure 3: Proportion of non-EU full-time students (2018)

Source: StuRents.com, hesa.ac.uk

Market Commentary

Allsop LLP - Anthony Hart, Partner, Residential Investment & Student Housing

It is important to rewind to the turn of the year; 2020 transaction volumes were set to be the highest on record. Confidence in the sector was high and built on solid foundations; a decade of strong performance, growing numbers of international applications and a seriously favourable demographic outlook here in the UK.

Transactions have somewhat ground to halt in light of Covid-19 but for good (short-term) reason. Providers of student housing have rightly focused their immediate attention on operational matters such as the health and safety of their students and how to deal with the contentious issue of rental payments.

Having overcome initial hurdles, it is unlikely the market will gather pace until there is some certainty regarding the start of Academic Year (AY) 2020-21. Right now, this is where the sector needs clarity to enable providers to make informed business decisions. Until we get to a point in the weeks ahead whereby providers can use facts to establish the impact of a delayed, or online start to AY 20-21, most will wish to sit on their hands.

There is an acceptance that student housing hasn't been immune to the issues posed by a global pandemic and indeed it has and will continue to inflict some short-term pain on landlords. Some will suffer greater than others, dependent on a range of factors. HMOs and the secondary market arguably less so, for example. But looking beyond AY 2020-21, it is quite conceivable the market will recover at every level very quickly. The fundamentals that underpinned market sentiment at the turn of the year haven't changed. In fact political issues in the US and the beaming example of our NHS might just encourage more international students than ever before.

Students want to return to university in September and new starters still want to go to university - UCAS numbers show as much. Investors still want to acquire student housing and belief in the asset class has not wavered. Matters outside of both the students and investors control will dictate when normality will resume - both want it just as bad. If 2020 witnesses a dip in student numbers and transaction volumes, expect 2021 to feel the full positive impact as higher education and student housing bounces back stronger.

Where the deal is right, the weeks ahead might not be such a bad time to buy.

The extracts above have been taken from our Quarterly Market Reports covering all major university towns and cities across the UK and Ireland.

To understand more about our market leading analytics Register Here.

About StuRents:

- StuRents is one of the leading proptech partners in the UK student accommodation space

- StuRents operates StuRents.com, the largest student-centric accommodation search platform, listing over 750,000 bed spaces nationwide

- Beyond search, StuRents facilitates integrated online tenancy signing, tenancy payments and app-based tenancy management solutions

- This unique, vertically integrated end-to-end solution underpins StuRents' data insights and research capabilities

Share

Article by

Head of Research at StuRents

Richard leads the StuRents research team, providing proprietary, platform-driven insights to help stakeholders make better-informed decisions about the market.